We don’t usually address geopolitical scenarios because they are often responsible for structural changes and must therefore be analyzed over very long time horizons. Furthermore, we admit we are not experts on the subject and therefore prefer to avoid commenting on scenarios now clouded daily by “dramas” (unfortunately not staged by actors) that “play out” mainly on social media. Nevertheless, we will attempt here an analysis limited to a geopolitical variable closely linked to macroeconomics and finance: global trade, which is entering a new historical phase, in which straits, raw materials, and the security of shipping routes matter more than the ideology of efficient globalization. The crucial point—in our view—is that the financial and geopolitical worlds are beginning to diverge.

For thirty years, the Western economy operated under the implicit assumption of abundance: smooth supply chains, abundant energy, free trade, and low logistics costs.

Today, however, nations are tending to stockpile strategic reserves, regionalize supply chains, militarize transit points, and sign bilateral emergency agreements. The most telling example is the agreement between New Zealand and Singapore to mutually guarantee fuel and food supplies in the event of global shocks. This agreement is certainly not unique: Australia recently signed a similar agreement with Japan to ensure the supply of rare earth minerals, fuels, and agricultural products in anticipation of potential crises. The European Union is considering the creation of regional fertilizer stockpiles amid fears of a food crisis. Governments and companies around the world are now quietly stockpiling essential goods.

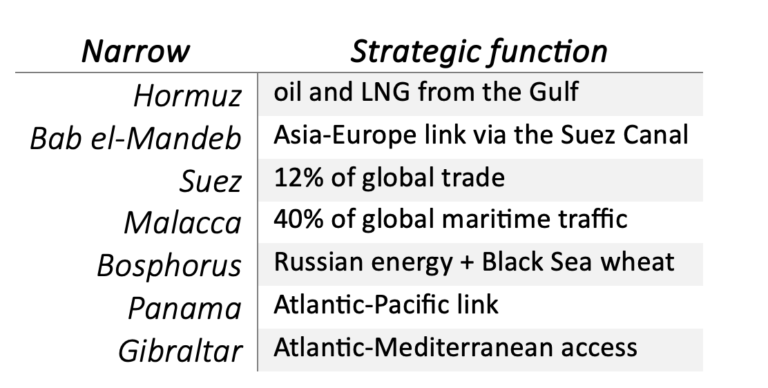

The geographical aspect of this new political and strategic approach maps out the sea straits of crucial importance for the transport of goods and raw materials. We are referring—and this list is by no means exhaustive—to:

• Hormuz,

• Bab el-Mandeb,

• Suez,

• Malacca,

• Bosphorus,

• Gibraltar,

• Panama.

which are no longer mere “sea passages,” but instruments of strategic pressure. Let us recall that in 1958 a UN convention established the principle of freedom of navigation, which remained in effect until 1982 when the so-called “Constitution of the Oceans” was signed in Montego Bay (Jamaica), establishing:

• maritime sovereignty of states;

• exploitation of marine resources;

• commercial and military navigation;

• protection of the marine environment;

• management of international straits.

This international convention arose from the fact that many countries sought to extend their sovereignty over the waters adjacent to their coasts for reasons of security and control of maritime traffic, as well as for the exploitation of marine resources such as fish, oil, and gas.

The two superpowers of the time, the U.S. and the USSR, possessed global fleets and, above all, nuclear submarines. Consequently, if every state had been able to restrict passage through its territorial waters, the American and Soviet fleets would have been trapped because many strategic straits would effectively have become “closed doors.” This led to the 1982 compromise under which the U.S. and the USSR accepted other countries’ sovereignty over territorial waters extending up to 12 nautical miles from the coast (approximately 22.2 km). In exchange, they secured freedom of transit for their submarines and military vessels through the seven most important straits.

The United Nations Convention on the Law of the Sea (UNCLOS), signed in 1982, entered into force in 1994, establishing—among other provisions—the payment of a toll only at man-made waterways such as Suez and Panama, with the exception of the Bosporus Strait, which is governed by the Montreux Convention (1936), which grants Turkey the right to collect a tax on vessels in transit.

All of this is changing in practice!

The most emblematic case is the Strait of Hormuz, which is now in the news spotlight. Before the crisis, approximately 20 million barrels per day passed through it, accounting for 20% of the world’s oil. Following the Israeli-American conflict against Iran, the Pasdaran have transformed the strait into a system of selective authorizations and illegal tolls; traffic is reported to have dropped to as low as 5% of previous levels.

The mechanism is interesting because it does not resemble a classic naval blockade: some ships pass through, others remain stationary; some pay in yuan or stablecoins, while others receive priority lanes for diplomatic reasons.

This brings about a radical transformation: the Strait of Hormuz is no longer merely a geographical point, but a political and financial infrastructure from which the entities that effectively control it benefit. But the truly worrying scenario is that this strait is becoming a model that countries controlling other straits are beginning to look to and draw inspiration from.

The global system can be viewed as a network of bottlenecks.

The historic shift is that these passages are no longer neutral (as they were until just a few days ago), but are being used as political leverage and exploited economically by charging transit tolls.

In essence, geography has become more important than finance because it is imposing selective deglobalization. The situation in all the straits listed above has concrete consequences:

• the Houthis are threatening Bab el-Mandeb with tolls modeled on the Iranian system;

• Indonesia is considering tariffs in Malacca;

• Panama has become a battleground between the U.S. and China;

• the Bosphorus is now an integral part of the Russia-Ukraine war.

The principle of “freedom of the seas” or freedom of navigation, established after World War II, is eroding.

Furthermore, we must not make the mistake of viewing control of these straits as a military issue and the exclusive domain of the few states bordering these maritime passages. Other actors and factors play key roles, ranging from insurance (for cargo and ships) to banks that finance trade (trade finance) and provide commercial credit; not to mention variables such as war premiums, freight rates, and navigation certifications.

Viewed from this perspective, Hormuz functions as a “risk transmitter.” If a route is classified as a war zone:

• insurance premiums skyrocket,

• banks freeze letters of credit,

• some companies stop sailing,

• the final cost is passed on to global inflation.

This is the true economic multiplier of the crisis, and it is a risk that could spread to other straits. Assuming these premises are valid, three possible economic consequences come to mind:

a) Structural inflation

If global trade becomes increasingly inefficient because it requires longer routes, leading to duplication of supply chains and the need for strategic reserves of essential materials, then the low-inflation model of the past 25 years could be over.

b) The end of the “just-in-time” approach

Companies will likely adapt by maintaining larger inventories, focusing on localized production and prudent logistical redundancy. Ultimately, this is a more expensive model than “just-in-time,” but a more resilient one.

c) The return of real assets

Even though markets continue to reward almost exclusively the digital world and AI, the true vulnerability of the global economy is becoming—and will increasingly be—material. Big Tech accounts for about 35% of the S&P 500, while energy and materials account for only 6%.

However, AI itself requires copper, lithium, gallium, cement, water, and a stable electricity supply.

In practice, the immaterial economy depends increasingly on the material one (ultra-material infrastructure).

In addition to the strategic importance of these sectors, the tactical—if not strategic—importance of certain investment themes is also emerging, such as:

• energy,

• mining,

• infrastructure,

• shipping,

• agriculture,

• utilities,

• defense.

For years, these sectors have been neglected because they were considered part of the “old economy.” Now they could return to or remain (defense) central.

The paradox is immediately apparent: the more the world becomes digital, the more it depends on vulnerable physical infrastructure.

AI depends on:

• data centers,

• energy,

• semiconductors,

• rare earths,

• copper,

• liquefied natural gas,

• maritime routes.

And all these supply chains pass through a few key chokepoints because they originate from just a handful of countries scattered across the globe.

This is why we must view the situation from a perspective far broader than a regional crisis, as we are rapidly transitioning from a world based on open globalization to one centered on resource security and control of strategic corridors.

Disclaimer

This post reflects the personal opinions of the Custodia Wealth Management staff who authored it. It does not constitute investment advice or recommendations, nor does it provide personalized consulting, and should not be considered an invitation to engage in transactions involving financial instruments.