The single entitled “Oro,” released in 1984, is perhaps Mango’s first real hit and could be the soundtrack to these days. Blogs and newspapers are now talking about nothing else: the new highs of gold, which has exceeded the psychological threshold of $4,000 per troy ounce. Few seem convinced that this is a speculative bubble: one above all is Ray Dalio, not to mention the announcements by American investment banks. Rather, it is argued that this rise is the result of various global uncertainties that are adding up or perhaps multiplying. Although well known, we list them here for clarity:

- ○ the trade war;

- ○ the wars in the Middle East and Ukraine;

- ○ US debt and repeated attacks on US institutions;

- ○ the US government shutdown;

- ○ European weakness.

These causes fuel inflationary fears on the one hand and flight from the dollar on the other, playing into the hands of the US administration, which is counting on a devaluation of the greenback to win the tariff war. The former are typically immunized with safe-haven assets: equities, precious metals (especially gold), the yen, and the Swiss franc. However, the stock market, which only seemed to emerge from its sluggish performance after the summer, was obviously affected by the tariff war (which suddenly seems to have been forgotten) as well as the situation in tiny Switzerland, which led investors to doubt the franc despite the country having the lowest debt-to-GDP ratio in the world. The yen is not held in high esteem due to political instability, which seems to be showing signs of improvement only following the recent election of Sanae Takaichi as leader of the ruling LDP party, which will lead her to become the country’s first female prime minister. But this does not seem to be enough to reconfirm the yen as a safe haven asset.

Gold remains, having certainly grown due to purchases by central banks at the expense of the dollar (we have said and read this a thousand times), whose reserves have even exceeded those in euros in value. But the post-summer growth was not due to the actions of central banks, but rather to purchases by passive funds. In our opinion, this is not a sign of strength supporting the upward trend because behind the demand for ETPs there may be (and probably are) retail investors who are driven in this case by FOMO (Fear-Of-Missing-Out), i.e., the fear of being left out of this gold rush, which is often a harbinger of bearish scenarios or outright crises.

Other key moments for the price of gold came during periods of chaos or uncertainty: it exceeded $1,000 following the 2008 financial crisis and $2,000 during the Covid-19 pandemic, while the $3,000 threshold was exceeded in March this year, shortly before Donald Trump’s “Liberation Day” tariffs sent financial markets into turmoil.

Nevertheless, we still believe in the continuation of the gold trend, comforted by recent data from the US Commodity Futures Trading Commission (CFTC) on hedge fund allocations, which currently hold a record amount of gold worth $73 billion. In short, the classic “herd behavior” that characterizes retail investors and shapes the latest peak of a speculative bubble does not seem to be the cause of the recent rises. There is also the latest quarterly statement from the World Gold Council, according to which the annual survey of central banks revealed that “95% of reserve managers believe that global central bank gold reserves will increase over the next 12 months.” In other words, there has been and will continue to be solid demand supporting the upward trend in gold.

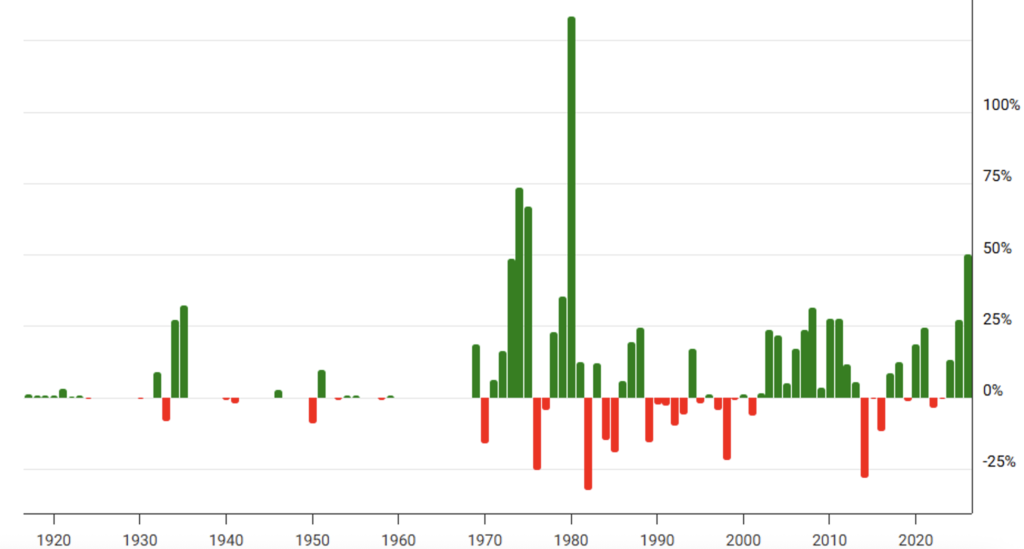

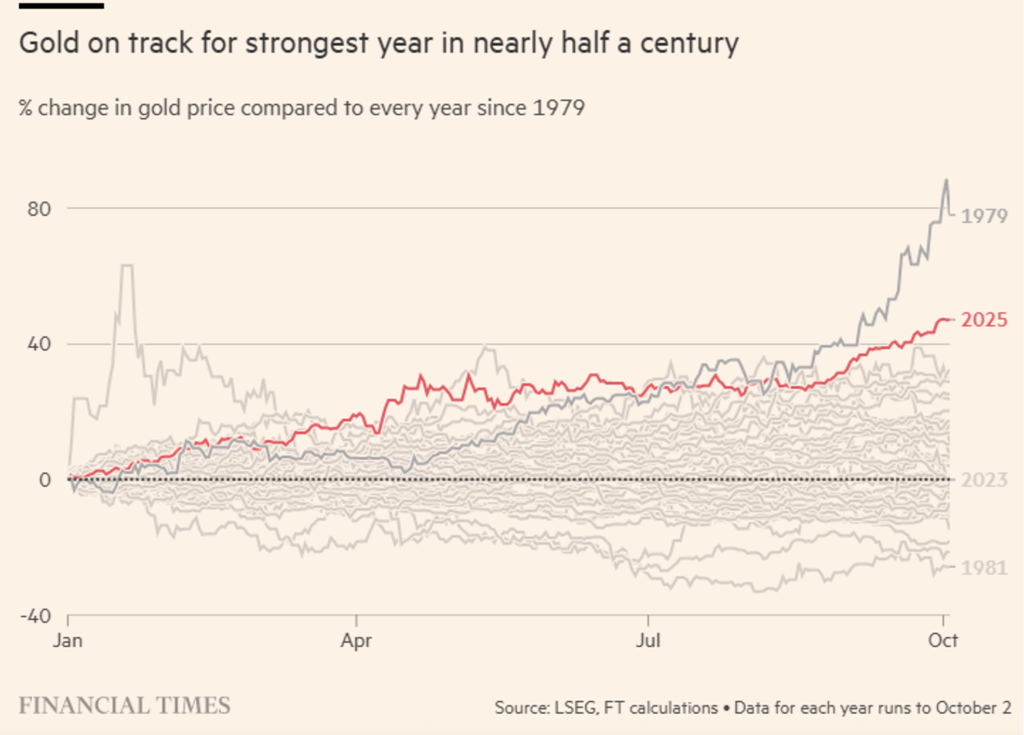

Finally, we have the comfort of data. We have already shown the inflation-adjusted gold price chart in our May 9, 2025, Insight, in which the yellow metal was already showing new highs compared to the 1979 peak, and obviously, these new highs have increased further to date (Figure 1). However, there is another way to adjust performance for inflation: analyze the performance of a financial asset for each year from January 1 to December 31 of each year. This is what is proposed in Figures 2 and 3. It is clear that there is at least one year (1979) in which the performance of gold is higher than that of 2025 (and by a long way: +133%), so we can conclude that there is still room for growth and that the growth potential of the precious metal is not completely unexplored territory.

There is also a new high for what we defined as digital gold in the above-mentioned In-depth Analysis: bitcoin. There are now forecasts of significant increases for this asset as well. However, in our opinion, the reasons for this are less solid. The fact that Trump is pro-crypto does not seem to us to be such an interesting reason. Instead, we believe that, thanks to the many characteristics it shares with gold, a strong upward push could come from central banks, which could accumulate bitcoin in addition to gold itself at the expense of the dollar. However, we do not see any clear indications on this point from either governments or central banks.

Figure 1. Spot price of gold. Monthly data from January 1915 to September 2025. Spot prices are adjusted for inflation using monthly CPI data (source: www.macrotrends.net).

Figure 2. Year-on-year performance of gold from 1915 to 2025. The 2025 performance refers to the end of September and is not annualized (source: www.macrotrends.net).

Figure 3. Cumulative performance of gold from January 1 to October 2 of each year since 1979 (source: FT, October 5, 2025).

Disclaimer

This post expresses the personal opinion of the Custodia Wealth Management staff who wrote it. It does not constitute investment advice or recommendations, personalized advice, and should not be considered an invitation to carry out transactions on financial instruments.