What better title than that of a famous Clash song to describe the clash between Switzerland’s top political institutions and UBS? By now, the conflict goes far beyond banking regulation: it calls into question the historic relationship between Switzerland and its leading financial institution, the Union of Swiss Banks. The crux of the matter is simple but potentially explosive: can a bank with assets exceeding Switzerland’s entire GDP still be supported by a state of just nine million inhabitants? It is worth noting, incidentally, that UBS has had assets exceeding the country’s GDP for several years now, well before the merger with Credit Suisse, and so the country has been living with a very high systemic financial risk for several years.

Following the rescue of Credit Suisse in March 2023, UBS has become an even more systemic bank, not only for Switzerland but for global financial stability. The takeover, orchestrated by the Swiss government to prevent international contagion, has, however, transformed UBS into an institution perceived as ‘too big for Switzerland’ – too big to be allowed to fail and perhaps even too big to be regulated within Switzerland’s current political and fiscal framework.

This is the source of the current conflict. The federal government wants to impose much stricter capital requirements on UBS, in particular by obliging it to fully capitalise its foreign subsidiaries. The aim is to prevent the state from having to intervene again with public guarantees or extraordinary support in the event of a future crisis.

UBS counters that such requirements would put it at a disadvantage compared to its American competitors, who are benefiting from relatively more permissive regulation. The bank argues that a capital burden of around $20–25 billion would reduce profitability, undermine its international competitiveness and could make a strategic review of its headquarters location inevitable.

It is against this backdrop that two main scenarios emerge.

In the first scenario, UBS remains in Switzerland. This would be the solution most consistent with the bank’s history, with the value of the ‘Swiss bank’ brand and with Zurich’s role as a global financial centre. Remaining would also allow the political, symbolic and reputational link between the Confederation and its leading banking group to be preserved. However, this scenario implies that Switzerland would have to accept living permanently with an enormous systemic risk: in the event of a crisis at UBS, the state’s fiscal capacity could prove insufficient without exceptional measures. This is precisely why the government is insisting on the capital increase.

In the second scenario, UBS moves its registered office abroad — probably to the United States — to benefit from a more favourable regulatory framework and greater geographical alignment with its international business. This possibility is currently being officially downplayed (by the bank’s top management), but is no longer ruled out. The board of directors is reportedly already exploring options for establishing a foreign domicile as a bargaining chip in negotiations with Bern, without yielding to the strong pressure from shareholders who are said to have already initiated the procedure for transferring the registered office abroad.

A potential transfer would have far-reaching implications. For Switzerland, it would mean losing part of its status as a global financial powerhouse, with significant symbolic, fiscal and geopolitical consequences. For UBS, on the other hand, it would mean freeing itself from a regulatory environment perceived as excessively cautious, but at the cost of very high political, reputational and operational costs. Furthermore, the historical value of the UBS brand remains closely associated with Swiss stability: separating the two elements could weaken one of the bank’s main competitive advantages in international wealth management.

The discussion becomes even more delicate when considering the historical precedent of bank bailouts in Switzerland.

In the case of Credit Suisse in 2023, there was formally no traditional ‘bailout’ (1) at the taxpayers’ expense comparable to those of the 2008 crisis in the United States or the United Kingdom. However, the Swiss Confederation and the Swiss National Bank made enormous liquidity facilities and public guarantees available. Specifically:

• the SNB provided over 200 billion Swiss francs in liquidity support;

• the federal government guaranteed up to 9 billion francs of potential losses on certain problematic assets transferred to UBS;

• extraordinary emergency guarantees were activated, implicitly backed by the Swiss taxpayer.

In the end, UBS did not fully utilize the government guarantees, and many of the lines of credit were repaid quickly. This allowed the government to argue that taxpayers did not suffer any definitive direct losses. However, the risk assumed by the public sector was enormous, and only the successful outcome of the integration prevented very high fiscal costs from materializing.

There is also the precedent from 2008, when the Swiss Confederation had already intervened to rescue UBS during the global financial crisis. At the time, the Swiss National Bank created a stabilization fund (“StabFund”) that purchased approximately $38.7 billion in toxic assets from UBS. At the same time, the Swiss government invested 6 billion francs in the bank’s convertible bonds. In that case, taxpayers did not incur any final losses—in fact, the federal government made a profit on the transaction—but once again, the public sector had to act as the guarantor of last resort for banking stability.

And this is precisely the crucial political point of the entire debate: even if the Swiss bailouts did not result in permanent net losses for taxpayers, the implicit risk transferred to the state was enormous. Today, the government wants to drastically reduce the likelihood of having to repeat a similar operation, because next time it could spell serious trouble (i.e., significant outlays) for the state and thus for taxpayers. UBS, on the other hand, fears that the price of this security will make it impossible to compete on a global scale.

The real strategic question, therefore, is not merely where UBS should have its registered office, but what economic model Switzerland wishes to adopt for the future: to continue being the home of a global systemic bank, or to voluntarily scale back national financial risk even at the cost of losing international prominence.

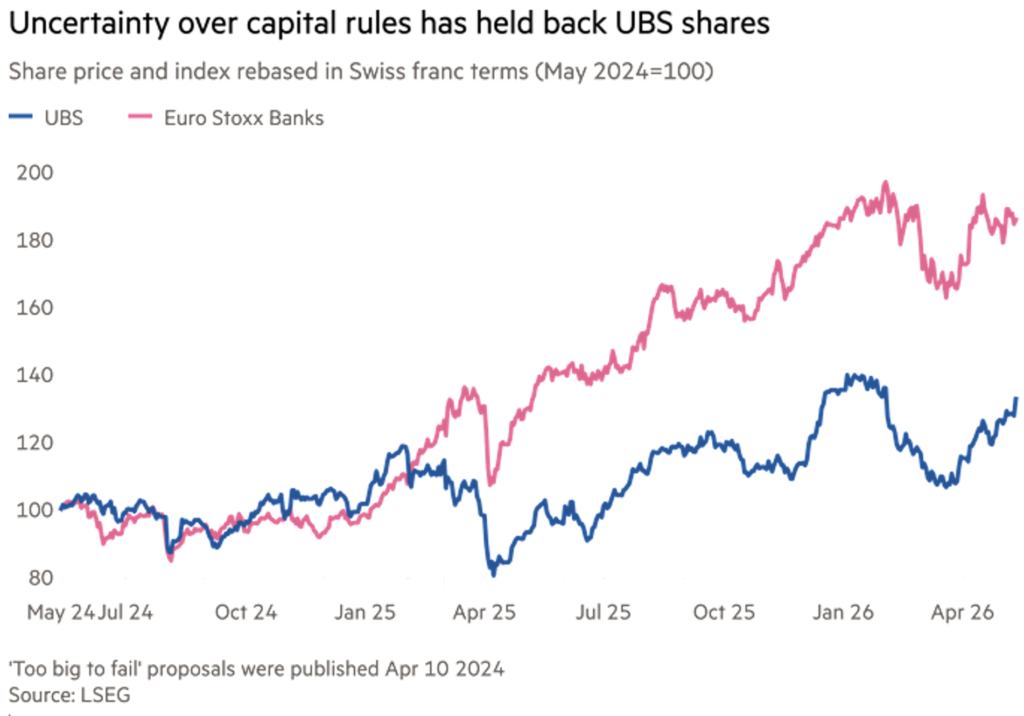

The issue is certainly not simple, and this suggests it will take time to understand the banking giant’s true positioning, which in the meantime—due to this complex situation—continues to underperform the European banking index (see chart).

It would likely have been better not to put the option of foreign domiciliation on the table right away, as it has transformed from a negotiating tool into an unpleasant threat that only hardens positions.

(1) A bailout is a financial rescue of a strategic company in distress through external intervention—typically by the government or the central bank—to prevent its bankruptcy and avoid systemic effects on the economy and/or financial markets.

Disclaimer

This post reflects the personal opinions of the Custodia Wealth Management staff who authored it. It does not constitute investment advice or recommendations, nor personalized consulting, and should not be considered an invitation to trade in financial instruments.