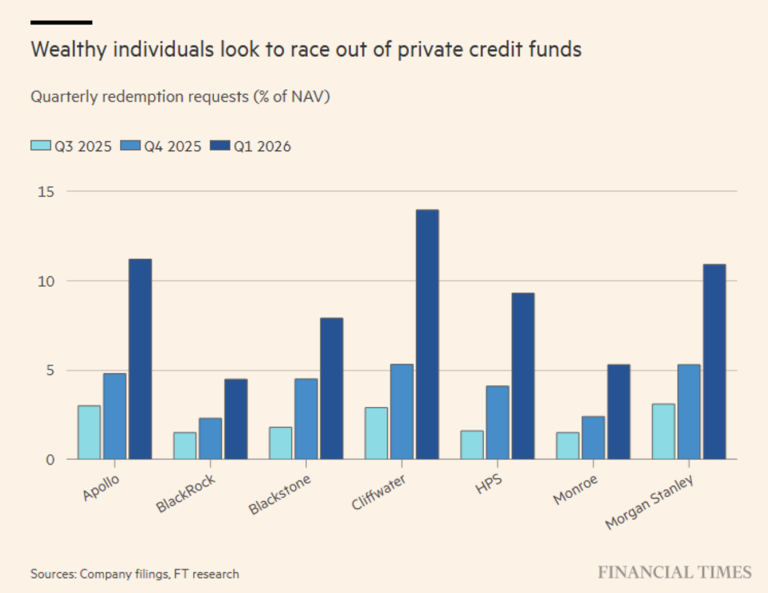

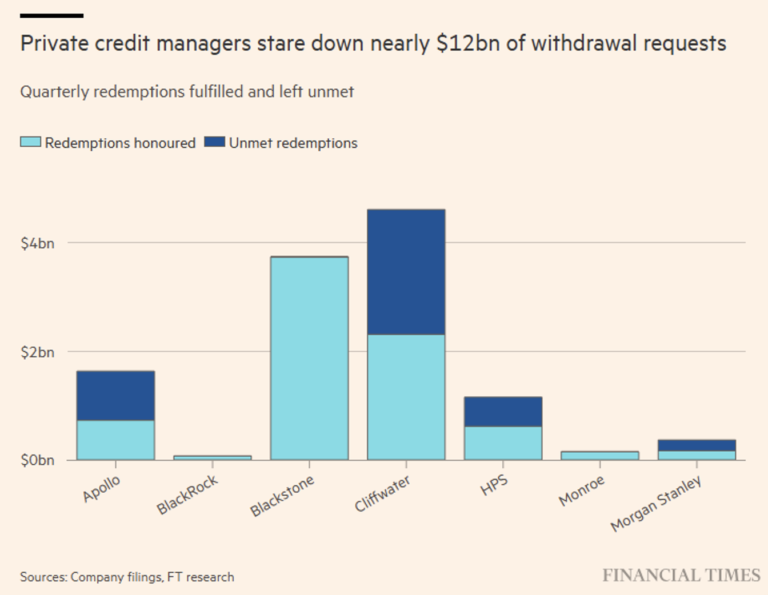

Where do we stand with private credit? Every new development in this area prompts us to provide updates. This week, Apollo Global Management is limiting redemptions because—as we have repeatedly noted—“semi-liquid” funds are revealing their structural trade-off: access to higher returns versus limited liquidity. High-net-worth individuals (HNWIs) are accelerating their redemption requests: ~$11.7 billion requested, but only ~66% fulfilled (see chart).

Liquidity is managed, not guaranteed. This is the mantra every investor should repeat to themselves.

In addition to the freeze on redemptions, Apollo has shown further signs of deterioration, such as its first monthly loss of -0.07% in over three years; trailing performance down to 7% (below the historical average); and a defensive rotation with reduced exposure to loans to software companies.

We have said and repeated this in various in-depth analyses: in private credit, market risk is always hidden from the investor because, without public quotes, it would be impossible to do otherwise. The risk must therefore be assessed and quantified according to other logics and variables, such as widening spreads (relative to listed credit); concentration risk (currently in software); and mismatched maturities.

If there is at least one positive aspect that this alarming situation in the sector has brought to light, one could first and foremost cite the shift in perception regarding this asset class, which is moving from “stable returns + low volatility” (a totally distorted view) to its factual definition: a form of illiquid credit with discretionary valuation and conditional liquidity.

The message for investors is clear: liquidity is merely an illusion (we would call it a “trap” if the term were not already reserved for other contexts), which necessitates a thorough examination of the redemption rules governing these investment vehicles. But here we find a second positive aspect: in our view, the management of redemptions has been impeccable and, far from harming the frustrated investor who received only part of the requested redemptions, has adequately protected remaining investors and will protect new entrants.

Disclaimer

This post reflects the personal opinions of the Custodia Wealth Management staff who authored it. It does not constitute investment advice or recommendations, nor does it constitute personalized consulting, and should not be considered an invitation to engage in transactions involving financial instruments.