Semi-liquid private debt funds are based on the same simple concept that characterizes commercial banking: not all account holders will withdraw their deposits at the same time, creating a liquidity crisis for the bank. In reality, in situations of panic (whether justified or not), a banking rush can occur, with the result that the bank is unable to meet its payment commitments. Recently, high redemptions have reappeared for two funds managed by Cliffwater, which received requests for 14% of NAV but decided to honor only 7% (the threshold allowed by the SEC is 5% but can be increased by an additional 2%, so everything is within the permitted limits) and Morgan Stanley, which reported redemption requests rising to 10.9% in the first quarter and that it would satisfy 45.8% of those requests.

Although meeting higher redemption requests is seen as a way to strengthen investor confidence in private credit and the liquidity of individual funds, the flip side of the coin cannot be overlooked, namely creating the expectation that funds can be fully redeemed in times of stress while increasing the fund’s leverage if outflows are financed with debt.

These dynamics develop when retail investors approach these asset classes without the necessary awareness of the risks, so that in a panic situation they rush to redeem their investments. As we have repeatedly stated, certain types of investment are only suitable for sophisticated investors, i.e., those who are able to carefully assess the risks. Consequently, in this Insight we intend to present the concerns of institutional investors about the sector.The risk that many large institutional investors (pension funds, sovereign wealth funds, endowments – e.g., American universities) currently consider to be most underestimated in private credit is not so much the default of individual loans as the risk of hidden correlation and systemic concentration among managers.

In other words, many funds are financing the same companies with very similar structures, creating a potentially systemic vulnerability.

The direct lending market is heavily concentrated on private equity sponsors, large credit platforms, and relatively limited pools of mid-market companies, i.e., companies between small and large in size (for a more precise definition, see, among others, this website).

It often happens that one fund leads the loan and other funds participate in the syndication club.

Typical example:

|

Company |

Lender |

|

PE-backed software company |

Apollo |

|

Participating tranche |

Blackstone |

|

Participating tranche |

Ares |

|

Participating tranche |

Blue Owl |

If that company gets into trouble, many funds suffer losses at the same time.

In private credit, there are many forms of interconnection:

• club deals

• co-investments

• secondary loan trades

• feeder funds

This means that risk is not independent between portfolios. A single problem can therefore spread rapidly among listed BDCs, semi-liquid retail funds, and closed-end institutional funds.

In recent years, private credit has mainly financed:

|

sector |

estimated weight |

|

software / SaaS |

very high |

|

tech services |

high |

|

healthcare services |

medium-high |

|

business services |

high |

This has happened because these companies have recurring cash flows, high margins, and active PE sponsors; but it creates a concentration of sector risk, so that if one sector gets into trouble (e.g., mid-market software), many portfolios are affected simultaneously.

Another little-discussed point concerns the leverage of credit vehicles. Many funds use credit lines secured by the fund’s own portfolio, and this can amplify losses because if the value of the portfolio falls, leverage automatically increases.

One of the reasons private credit has grown so rapidly is that it appears less volatile than public (i.e., listed) credit. But this stability often stems from quarterly valuations produced using internal models and the absence of continuous trading.

In this context, when shocks occur, volatility emerges all at once.

We have already seen this in the past with real estate funds (especially American ones) in 2008, British ones in 2016, with gating in real estate funds in 2020, and with CDOs.

Large investors are primarily monitoring the percentage of loans under review, the number of covenant breaches, the volume of PIK interest (payment in kind, i.e., capitalized interest), BDC discounts relative to NAV, and secondary transactions on loans. Listed BDCs are often seen as a warning sign for the private market.

In addition to concentration risk, there are other risks worth mentioning and analyzing, and we will do so by drawing a parallel between the current market situation and the one that preceded the subprime bubble burst.

The comparison between private credit today and the CDO market before the 2008 financial crisis does not mean that the same scenario is repeating itself. The structures are different and the banking system is much more regulated. However, some economists and regulators see structural similarities in the mechanisms of risk and contagion.

The analysis focuses on four main aspects.

Before 2008, many credit exposures were securitized and transferred from banks to structured vehicles (CDOs, SIVs) and then to institutional investors. Today, something similar is happening but with different instruments.

|

Before 2008 |

Today |

|

banks → CDOs |

banks → private credit funds |

|

structured credit |

Direct lending |

|

SPV |

funds and BDCs |

After the global financial crisis, much stricter regulations were introduced:

• Basel III

• higher capital requirements

• limits on leveraged loans

This has made it less convenient for banks to hold risky loans on their balance sheets: today, they originate fewer loans that fuel leverage due to regulation, while private credit has filled that void. The result is a huge parallel credit market that is less regulated and less transparent. However, banks remain indirectly involved in this process because they provide loans (and therefore leverage) to private debt funds secured by the loans themselves. JPMorgan’s recent decision to write down private loans given as collateral following recent events involving giants such as Apollo, Blackrock, and Blue Owl shows that even though leverage has decreased, it remains a sensitive issue. For the time being, this decision by the American investment bank has not resulted in requests for additional margins, but it certainly represents a tightening in the granting of further leverage. Other banks have not followed suit, but JPMorgan’s stance highlights the real risk of contagion in the event of critical scenarios related to the asset class in question.

The speed of growth is one of the indicators that concern regulators.

Private credit has grown from around $500 billion in 2015 to over $2 trillion today. Much of this growth has come in the last five years thanks to low interest rates, demand for yield, and allocations from institutional investors.

Very rapid growth often coincides with deteriorating credit quality, compressed spreads, and weaker covenants.

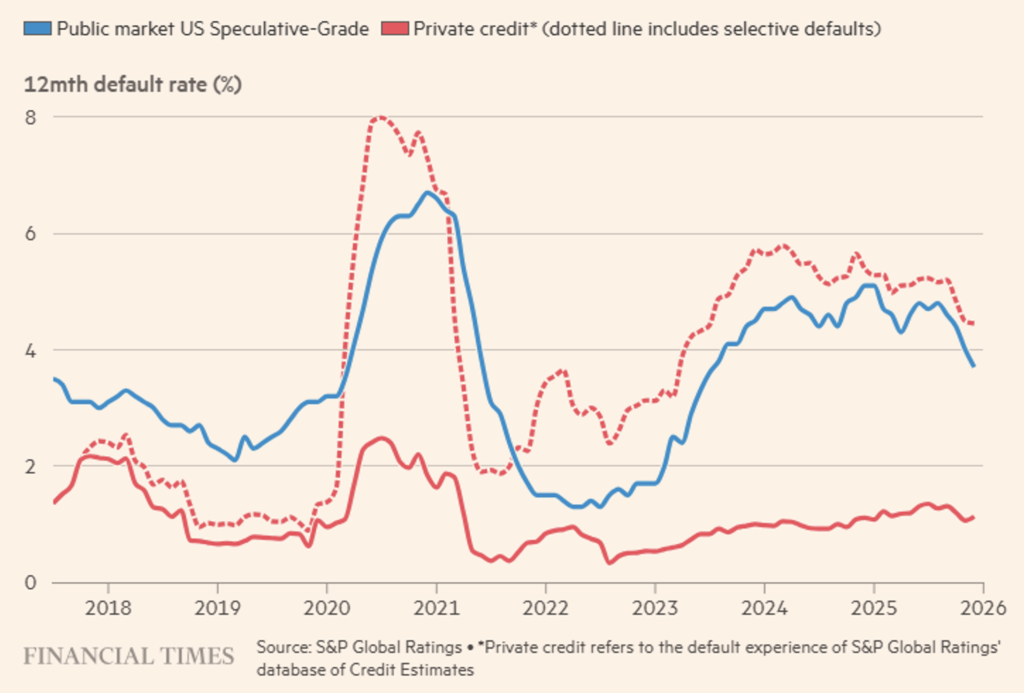

With regard to the deterioration in creditworthiness, we would like to highlight the recent position taken by Partners Group, which calls for the default rate on private loans to be recalculated according to the standards used to assess listed debt. The chart below (see Figure 1) is very telling.

In addition, Glendon Capital Management states that the debts in Blue Owl Capital Corporation’s portfolio are overvalued compared to similar securities traded on public markets. In particular, it notes that riskier junior tranches are priced significantly higher than the recent market prices of safer senior tranches issued by the same companies: a clear inconsistency. This situation obviously does not only affect Blue Owl: the loan portfolios analyzed at various BDCs—including those sponsored by KKR and BlackRock—report loss rates of less than 0.1%, which is misleading, given that companies that resort to private credit are inherently weaker and have been forced to turn to private credit after being rejected by public markets. The comparison becomes even more stark when one considers that yields on junior high-yield bonds, currently below 7%, are consistently lower than senior private credit loans, which typically yield around 10% or more.

Figure 1. Default rates in private credit appear much higher if borrowers are assessed according to public market standards.

In CDOs, the problem was the complexity of the structures and rating models. In private credit, opacity stems from the absence of a liquid secondary market, model-based valuations, and quarterly reporting. This creates a dynamic called NAV smoothing, which results in seemingly stable prices because they do not move on a daily basis, volatility that appears low, and the possibility of sudden price revisions. For this reason, many analysts look to listed funds (BDCs) as an early indicator.

In terms of economic incentives, we know that banks earned money on CDO structuring fees, while in private credit, managers earn money on management and origination fees. When the market grows rapidly, there is a risk that the pressure to allocate capital will lead to less rigorous credit risk assessment, higher leverage, and covenant-lite.

Private credit is a hold-to-maturity market. This means that prices are not continuously “discovered” by the market and liquidity can evaporate quickly. In fact, if many investors wanted to sell loans at the same time, the secondary market might not be able to absorb them easily and prices could fall rapidly.

That said, we note that there are important differences with the pre-crisis phase of 2008. First of all, there is a lower level of leverage in the banking system and therefore less propellant to trigger rapid and painful contagion; loans that are less complex than CDOs, structured loans that have been purchased by more sophisticated (institutional) investors, even if – as always happens – followed by retail investors, who are one of the reasons for concern.

Therefore, the main risk is not a systemic banking crisis, but rather a significant depreciation of private credit, resulting in higher yields, portfolio write-downs, and lower fund inflows.

In summary, the parallel with CDOs does not concern the technical structure, but the dynamics of the cycle, whose expansionary phase is characterized by:

• strong growth of a new asset class

• abundant capital

• compression of credit standards

• underestimation of liquidity risk

When the cycle changes, the market suddenly discovers the true price of risk.

The macro variable that many institutional investors consider most critical for private credit is not the level of defaults, but debt refinancing (refinancing risk) over the next 3-5 years.

In other words, the real risk is the “wall of maturities” of debt originated during the years of low interest rates.

Between 2021 and 2022, a large number of private equity and direct lending transactions (i.e., outside the banking system) were structured with very low rates, high leverage, and very high valuations.

The typical structure of the loans provided for an average duration of 5-7 years, minimal amortization, or even a single final repayment (maturity wall).

This means that a large number of loans will have to be refinanced between 2026 and 2029, and this will happen at an increasing cost.

Many loans were originated with terms such as SOFR+450bps ≈[5.6]%, where SOFR is the Secured Overnight Financing Rate. Today, even with falling rates, the structure is more like SOFR+[550,650]bps ≈[8.10]%.

Therefore, the cost of debt for many companies may double at the time of refinancing. Many sponsor-backed loans, i.e., loans granted to companies that are controlled, owned, or managed by a financial sponsor, typically a private equity fund, have been structured with Debt/EBITDA ratios of around 5/7x and EBITDA/Interest (interest coverage) ratios of around 2/3x. If the cost of debt increases significantly, interest coverage falls and refinancing becomes difficult. When a company is unable to refinance its debt, it often resorts to what is known as “extend and pretend,” i.e., extending maturities, capitalizing interest, and even revising covenants. In the short term, default is avoided, but in the long term, leverage is likely to increase and the repayment value to decrease. More drastic measures available to sponsors include injecting new capital, restructuring debt, and even selling the company to creditors. Historically, in times of stress, the latter option has become more common. Unfortunately, the peculiar characteristic of private debt is that as long as interest is paid, problems smolder under the ashes, never emerging gradually, but only as deadlines approach, when they suddenly reveal themselves in all their severity.

Finally, let’s look at why private credit is a particularly suitable asset class for institutional investors. First of all, because these investors are very sophisticated and constantly monitor certain risk factors such as:

1. portfolio maturity wall

2. percentage of covenant-lite loans

3. companies with stagnant EBITDA

4. level of PIK interest in funds

5. implicit loan-to-value relative to PE valuations

If you don’t understand what we’re talking about, it means you’re not a sophisticated investor and therefore it’s advisable to steer clear of certain investments.

Many institutional investors have return targets that are difficult to achieve with traditional assets, typically:

pension funds 6–7%

endowments 7–8%

insurance 5–6%

Investment grade bonds often offer less. Private credit, on the other hand, offers higher spreads, variable returns, and yields of between 8 and 12 percent. This makes it very attractive for strategic allocation. In addition, private credit has certain characteristics that appeal to investors, such as:

1. structural protection

• senior secured loans

• covenants

• asset guarantees

2. attractive returns with

• quarterly coupons (stability)

• variable rates

3. relatively low correlation with public (listed) markets.

For many institutional portfolios, private credit is seen as a substitute for high-yield bonds.

Private credit is also growing because private equity is growing, which should be an investment area for institutional investors. Almost every PE transaction requires:

• senior debt

• unitranche

• mezzanine

If private equity continues to expand, the need for private credit automatically increases. In addition, the sector is expanding as new segments emerge, such as:

• asset-based lending

• infrastructure credit

• NAV financing for PE funds

• specialty finance

• consumer lending platforms

This broadens the investable market but increases sophistication. In recent years, semi-liquid funds, BDCs, and wealth management products have grown significantly.

Large managers (Blackstone, Apollo, Ares, Blue Owl) are strongly pushing for the democratization of the asset class, i.e., they are becoming credit selectors for retail investors, and if retail capital continues to flow in, the market will grow even faster. Many analysts predict a path similar to this:

Year Estimated size

2015 ~$500 billion

2020 ~$1 trillion

2025 ~$2 trillion

2035 $5–10 trillion

Of course, this depends on economic cycles, default trends, and regulation. Based on all of the above, we expect the sector to continue to grow, but with more visible stress cycles than in the last ten years.

Disclaimer

This post expresses the personal opinions of the Custodia Wealth Management staff who wrote it. It does not constitute investment advice or recommendations, personalized advice, and should not be considered an invitation to carry out transactions in financial instruments.