Although the fourth Gulf War is currently dominating the headlines, we continue to focus on news concerning a sector that is entering a crisis and could (and here the conditional is a must) trigger a real systemic crisis: private debt, which we have repeatedly discussed in previous Insights.

Private retail credit: slowdown in fundraising, increase in redemptions, and systemic implications

This asset class is going through a period of significant tension. The two main recent developments—Blue Owl’s suspension of redemptions on an unlisted fund and the $1.7 billion in net outflows in the first quarter from Blackstone’s Bcred fund—signal a possible regime change in the sector’s flows.

The growth model of recent years, based on steady inflows from non-institutional investors into “semi-liquid” vehicles, is now being tested by slowing new inflows, increased redemption requests, greater sensitivity to illiquidity risk, compressed return expectations in a context of falling rates (at least this was the scenario before the new Gulf War), and increased defaults.

In recent years, private credit has been one of the drivers of expansion for large alternative platforms. Vehicles such as Bcred (Blackstone), Apollo Debt Solutions, funds managed by Ares, Blue Owl, and HPS (BlackRock) have raised hundreds of billions from financial advisors, family offices, and HNWIs. These funds are structurally invested in illiquid loans but allow periodic exit windows (typically up to 5% of NAV per quarter). The model works as long as inflows offset or exceed redemptions and portfolio liquidity, including credit lines, acts as a buffer. The system is therefore heavily dependent on stable retail sentiment, which is primarily responsible for inflows and outflows (and this applies in general, not just to this sector at this time).

Investors (especially retail) are selling exchange-traded private credit funds as they record losses on impaired loans and concerns grow that artificial intelligence could disrupt the software companies that these funds have financed (including the AI industry itself).

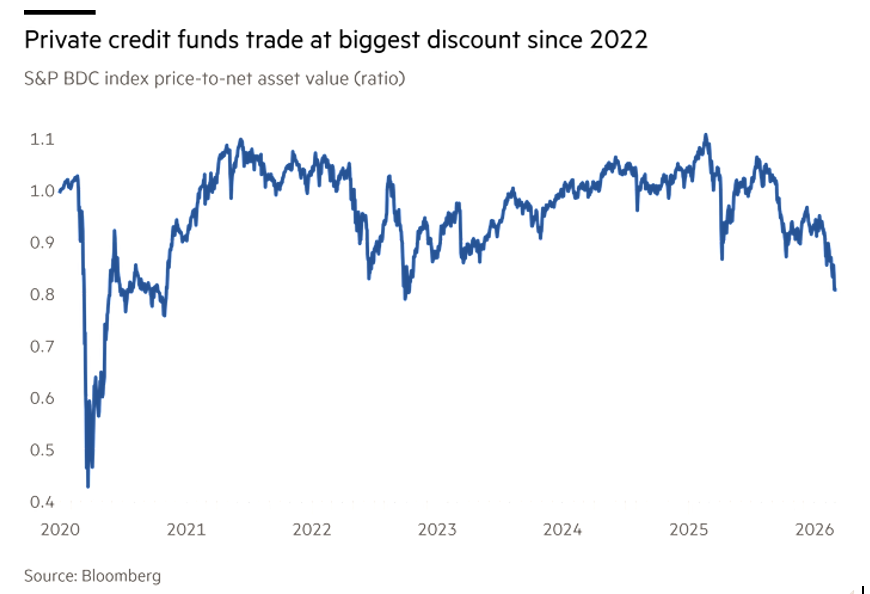

These vehicles, known as Business Development Companies (BDCs), which are the basis for the sector’s growth (see Figure 1), are trading at around 82 percent of their asset value, the largest discount since the end of 2022 (see Figure 1) and a sign that investors believe the funds will face further difficulties, according to Financial Times calculations based on the S&P BDC index.

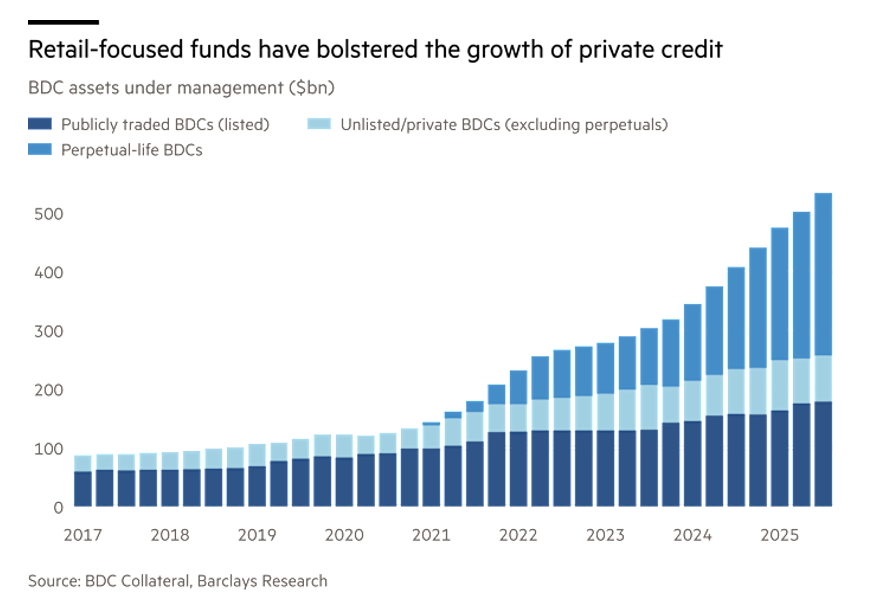

Figure 1. Breakdown of the main BDCs subject to investment.

Figure 2. Discount of funds listed on private debt.

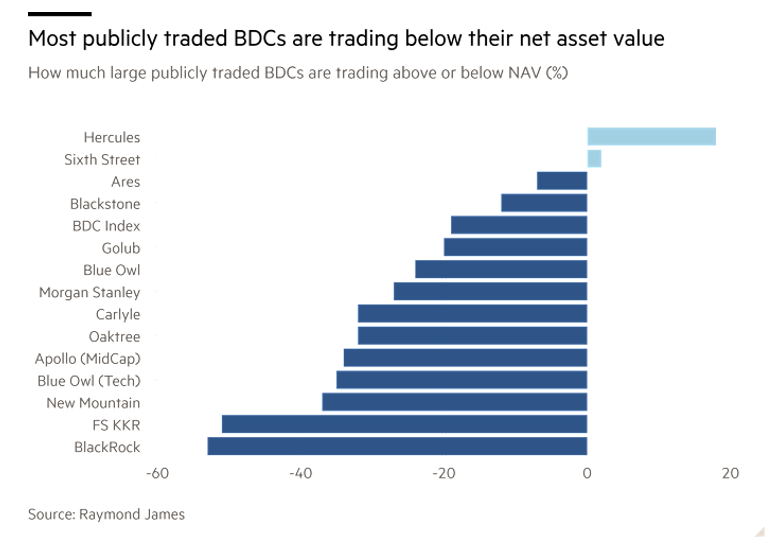

The decline in value of these BDCs (see Figure 3), which were trading at over 100 cents on the dollar of net asset value last September, has cast a shadow over the entire private credit industry (currently worth $2 trillion), increasing pressure on unlisted private credit funds that are facing an increase in redemption requests.

These vehicles, known as semi-liquid funds, have been a major growth driver for large private investment groups, including Blackstone, Ares Management, and Blue Owl, generating highly profitable management fees and helping to quadruple assets in BDCs since the end of 2020.

The decline in BDCs began last September when the Federal Reserve began cutting interest rates, reducing the yields offered by loans, which generally move in line with borrowing costs. The collapse, reported and emphasized by the media, of two automotive companies—First Brands and Tricolor—in the same month fueled concerns about corporate credit quality and underwriting standards.

Sales of BDCs accelerated again after a series of loan write-downs in the past two weeks by several large funds, including vehicles managed by KKR, BlackRock, New Mountain, Apollo Global, and Blackstone, which reduced the value of loans held in their portfolios. Funds managed by BlackRock, KKR, Morgan Stanley, and Apollo also reduced the dividends distributed by their vehicles.

Many HNWIs had been attracted to this segment by the high dividends offered, with total annualized returns exceeding 8 percent over the past decade, according to S&P Global.

The recent dividend cuts, coupled with asset sales by some funds, have reignited fears of a negative phase in the credit cycle in the private credit sector.

Figure 3. Market valuations of BDCs for major players in the private debt market.

How these funds work

From a technical standpoint, the main risks are concentrated in four structural dimensions of the business model: credit quality, liquidity mismatch, interest rate dynamics, and asset valuation.

Private credit has largely financed sponsor-backed companies (LBOs), software and technology companies, roll-up e-commerce platforms, and highly leveraged mid-market companies.

Many loans were originated between 2019 and 2022, in a context of very low rates, high valuations, and weaker covenants. As rates rise, companies’ debt service ratios deteriorate, EBITDA grows less than expected, and the risk of payment default or restructuring increases.

Several funds have had to write down loans, a sign that credit quality is under pressure.

Most private credit loans are variable rate (SOFR + spread). Between 2022 and 2023, high rates initially favored funds with higher coupons and high distributions for the benefit of investors. At the current stage, however, two opposing effects are emerging, caused by two different scenarios in interest rate dynamics: if rates remain high, we will see greater stress on borrowers and a consequent increase in bankruptcies; if, on the contrary, rates fall, then funds will reduce their returns and squeeze dividends.

The sell-off began when the Fed started to cut rates, in anticipation of declining fund yields.

Many retail private credit funds are semi-liquid, which means quarterly or periodic redemptions against illiquid underlying assets (private loans).

The typical structure of these funds’ portfolios is 5-7 year loans on the asset side with quarterly repayments of fund units.

If redemptions increase, funds may be forced to sell loans at a discount due to the illiquid market for these assets. This can generate a contagion effect among funds.

In private credit, there is no continuous market price. Valuations are based on internal models, comparables, and DCF. This makes the NAV of funds less volatile than listed financial instruments, where market risk becomes apparent. This can create the illusion that the funds are low risk, which is obviously not the case because risk has many facets: in addition to price fluctuations (market risk), there is interest rate risk, credit risk, and liquidity risk, and it is precisely these that matter in the private credit sector, risk factors that only institutional investors can adequately assess.

When listed funds (BDCs) trade well below NAV (currently 82%), the market is implicitly saying that NAV is probably too optimistic, implying a possible downward revision of portfolios.

Finally, concentration risk should not be overlooked. An emerging issue concerns exposure to SaaS software, technology, digital platforms, and e-commerce aggregators: the case of Medallia and companies selling on Amazon highlights that several problematic loans are concentrated in these segments.

Private credit has not experienced a true recessionary cycle since its post-2015 boom. Possible signs of the beginning of a cycle, which by definition implies a phase of decline, include loan write-downs, dividend cuts, discounts on listed vehicles, and an increase in credit restructurings. This does not necessarily imply a systemic crisis, but it does indicate that the sector is entering the first phase of stress in the modern credit cycle.

The Blackstone case: first real test of net outflows

In the first quarter, we saw a net outflow of approximately $1.7 billion for Bcred ($82 billion in assets). Redemption requests reached 7.9% of assets, exceeding the 5% threshold that allows for restrictions. Blackstone avoided blocking redemptions thanks to a direct investment of $400 million by the company and its employees and the fund’s tender offer structure, which allowed it to manage requests without invoking liquidity restrictions.

However, new commitments of approximately $2 billion and redemption requests of approximately $3.7 billion resulted in a negative balance of inflows, which is a structural, not episodic, signal.

Since Bcred generates approximately 13% of the group’s total fees (1.2 billion in 2025 between management and performance fees), the dynamics of cash flows are a topic of great interest to the group’s profitability.

The Blue Owl effect: reputational risk

Blue Owl’s decision to permanently suspend redemptions on an unlisted fund had a significant psychological impact, making financial advisors more reluctant to recommend the product due to uncertainty and increased requests for clarification from clients concerned primarily about the structural illiquidity of the asset class. We believe this is the main reason why we argue that the retail market should be prohibited from investing directly in this asset class: a lack of understanding of all the dimensions of risk associated with an investment.

The closest precedent is the Breit (Blackstone Real Estate) case in 2022, when redemption limits fueled a negative reputational cycle despite solid performance. A similar mechanism is now occurring in private credit.

Assessments and outlook

The Blackstone and Blue Owl cases have triggered a series of already tangible consequences, such as a slowdown in fundraising, with sales of funds from various firms falling by up to 70% in January compared to the monthly average for the previous year. In addition to Bcred, which raised $1.1 billion in the first two months of 2026 compared to over $1 billion per month in 2025 (practically halving), Apollo Debt Solutions recorded monthly placements 72% lower than last year’s average. We are therefore seeing a potentially destabilizing combination: a slowdown in inflows with an increase in redemptions.

It is clear that semi-liquid funds have an inherent mismatch, with illiquid private loans on the asset side and commitments to repay on a periodic basis (usually quarterly) on the liability side. As long as inflows exceed repayments, the system is self-sustaining, but when net repayments become negative, liquidity margins begin to erode.

To address this cash flow mismatch, private credit funds can resort to bank credit lines, the sale of more liquid loans, the use of the manager’s proprietary capital (all options that have a financial cost), or the possible limitation of repayments with the resulting reputational risk.

In this context, to which must be added the macroeconomic and financial framework linked to the Fed’s interest rate policy, at least three different scenarios can be envisaged:

Scenario 1 – Stabilization

• Outflows normalize.

• Liquidity structures hold up.

• The sector experiences only a temporary slowdown.

Scenario 2 – Persistent outflows

• Redemption windows generate recurring pressure.

• Managers begin to sell assets to generate cash.

• Compression of yields and fees.

Scenario 3 – Reputational shock

• Further redemption freezes.

• Contagion effect among similar funds (exacerbated by concentration risk).

• Structural review of the private credit retail model.

The third scenario is obviously the most worrying, not so much because of the losses suffered by investors and the downsizing of the sector, but because of the contagion effect it could create. It should be remembered that speculative bubbles burst when unsustainable debt somewhere in the system is not repaid. The strategic implications of this situation are:

1) for managers, the need to strengthen communication on liquidity and prudent management of buffers, together with greater discipline in credit selection;

2) for investors, an awareness of structural illiquidity (which would not justify direct retail investment in any case), resulting in consistent investment time horizons and a downsizing of tactical exposure with a more risk-weighted asset allocation;

3) for the sector, a potential downsizing of retail growth (if not a “healthy” degrowth) and greater polarization towards operators with stronger brands and balance sheets, even if this may not necessarily have positive implications.

In conclusion, we believe that recent developments do not yet constitute a systemic crisis, but represent the first concrete test of the retail private credit model in a net outflow phase.

The critical issue is not the solvency of portfolios, but rather the resilience of the liquidity structure in the face of negative expectations.

If the flow of redemptions continues for several quarters, the industry could enter a phase of structural adjustment, with less reputational leverage and greater emphasis on liquidity risk management.

Private credit remains a core asset class in alternative allocation, but the phase of linear growth driven by retail seems to have reached a point of discontinuity.

The risk in private credit today is not so much a single default, but rather a combination of four factors:

1) highly leveraged loans

2) increased cost of capital

3) liquidity mismatch in retail funds

4) valuations potentially lagging behind the market

If these dynamics persist, it is likely that in the coming years we will see more distressed exchanges, growth in the secondary market for private loans, and greater regulation of semi-liquid funds. Institutional investors are actually concerned about the risk of hidden correlation and systemic concentration among managers because many funds are financing the same companies with very similar structures, creating a potentially systemic vulnerability.

We reserve the right to explain in a subsequent post the approach of professional investors to this asset class, especially in terms of risk analysis, and to draw a “forced” parallel between these assets and CDOs (the cornerstone of the subprime crisis) to understand how real the possibility of systemic risk is.

Disclaimer

This post expresses the personal opinion of the Custodia Wealth Management staff who wrote it. It is not investment advice or personalized advice and should not be considered an invitation to carry out transactions on financial instruments.