Last Wednesday, the Financial Times published an article documenting a sharp increase in private investment in nuclear fusion: in 2025, 43 rounds of financing were recorded for $2.3 billion, the highest level since 2021. The reason is simple: investors believe that fusion—abundant, cheap, and emission-free energy—is moving from pure research to an industrial engineering phase.

The key points that have attracted the attention of many investors and will increasingly attract it in the future—we predict—are:

• Start-ups are beginning to go public via SPACs, a sign of the sector’s maturity; examples include General Fusion and TAE Technologies.

• Companies are moving from simulations and slides to building very expensive physical prototypes.

• No company has yet achieved commercial viability, but several promise electricity by 2028-2030, a scenario that is perhaps a little too optimistic, leading to huge valuations for technologies that are still far from generating revenue.

However, what is convincing a certain segment of investors is the transformation of the sector, which is no longer just academic research but a global industrial gamble.

For decades, the problem of fusion has been threefold:

1. confinement of plasma (superconducting magnets)

2. achieving sufficient temperature and density (Lawson criterion)

3. obtaining net energy gain (industrial Q>1)

In the last 5-7 years, there have been simultaneous advances in HTS superconductors, numerical simulations, and high-energy lasers, which has changed the perception of technological risk. Investors are therefore financing the most expensive phase: turning physics into engineering.

In 2022-2023, the National Ignition Facility achieved the first fusion reaction with scientific net energy gain (more energy produced in the reaction than in the fuel). This result is not yet commercial, but it has demonstrated that the physics works and has helped to stimulate much of the current venture capitalist and industrial investment, triggering a race to build compact tokamaks (HTS superconductors), a new generation of much smaller reactors thanks to REBCO magnets. The most relevant projects in this field are:

• Commonwealth Fusion Systems, SPARC (USA)

• Tokamak Energy, ST-E1 (UK)

• ENN, BEST tokamak (China)

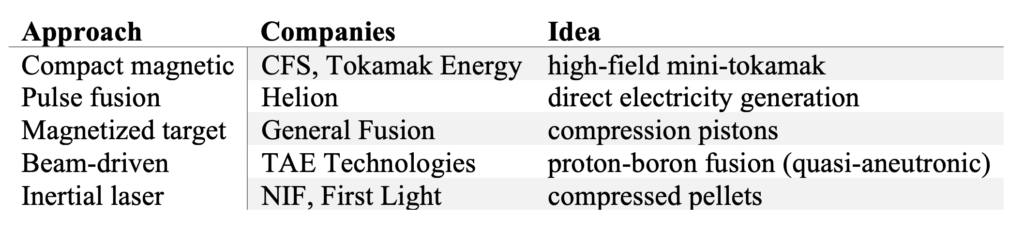

and all have set themselves the goal of building an electricity grid in the 2030s. This pioneering approach is complemented by other projects, which we summarize briefly in the following table:

Fusion has become a strategic energy technology, like nuclear power in the 1950s or semiconductors in the 1980s, moving from international big science to national industrial competition. The real obstacle is no longer physics, i.e., trying to understand how nuclear fusion works; the main problems are engineering ones:

• neutron-resistant materials

• robotic maintenance

• tritium production

• magnet costs

• grid load capacity

in order to build the power plant. After seventy years of uncertain scientific research, the theoretical obstacle can now be said to have been overcome; a decade of competitive industrial development now awaits us. This is why investors are getting involved, not because the development of nuclear fusion at an industrial level is guaranteed, but because for the first time there is a plausible timeline towards clean electricity that can be produced and sold with this new technology.

Disclaimer

This post expresses the personal opinion of the Custodia Wealth Management staff who wrote it. It is not investment advice or recommendations, nor is it personalized advice, and should not be considered an invitation to carry out transactions on financial instruments.