A major fine wine investment company known as Oeno House once boasted around 3,000 clients and promised double-digit returns on invested capital. Today, it is closing its doors within a matter of days. To understand what happened, we need to delve into the murky world of fine wine investment, where there is no financial protection when things go wrong. Dozens, perhaps hundreds, of people fear substantial losses after Oeno House’s subsidiary, Oenofuture Limited, ran into trouble amid widespread complaints of mismanagement and poor communication, as well as allegations of fraud (which have yet to be proven). Total losses could amount to millions.

The recent sudden closure of the business has revealed a much more problematic picture than many investors expected, with an industry that has transformed from an opportunity for returns into a situation fraught with significant losses. It is unclear whether the money is tied up in wines that have lost much of their value or whether the proceeds from sales were spent when they should have been returned to investors. Similarly, it has not yet been established whether the company deliberately misled investors over a period of time or simply failed to fulfill its responsibilities to customers after finding itself in difficulty.

In 2015, the situation was very different: riding the wave of the global boom in fine wine investment fueled by the Far East, Oeno was launched with the promise of high returns and a comprehensive personalized service. To work in the wine industry, you need to be involved in every aspect of it: trading, investing, sales, collecting advice, and understanding the retail market. In addition to the UK, Oeno had a presence in Portugal, Italy, Spain, Australia, and America. It was named “Best Global Wine Investment Company” by International Investor Magazine for three consecutive years.

Although the precise reasons for Oeno’s failure are unclear, one underlying problem is the notoriously volatile nature of the fine and collectible wine market, which is estimated to be worth around £20 billion worldwide. In the UK, investments in fine wines are not regulated by the Financial Conduct Authority (FCA), which means there is less transparency and more risk of losing money. If a company goes bankrupt, investors do not have the protection they would have if their money were deposited in savings accounts.

The market boomed during and after the 2008 global financial crisis, when interest rates plummeted and savers sought higher returns from alternative assets such as fine wines, art, and jewelry. According to FCA estimates, 3.4 million people in Britain held such investments in 2024.

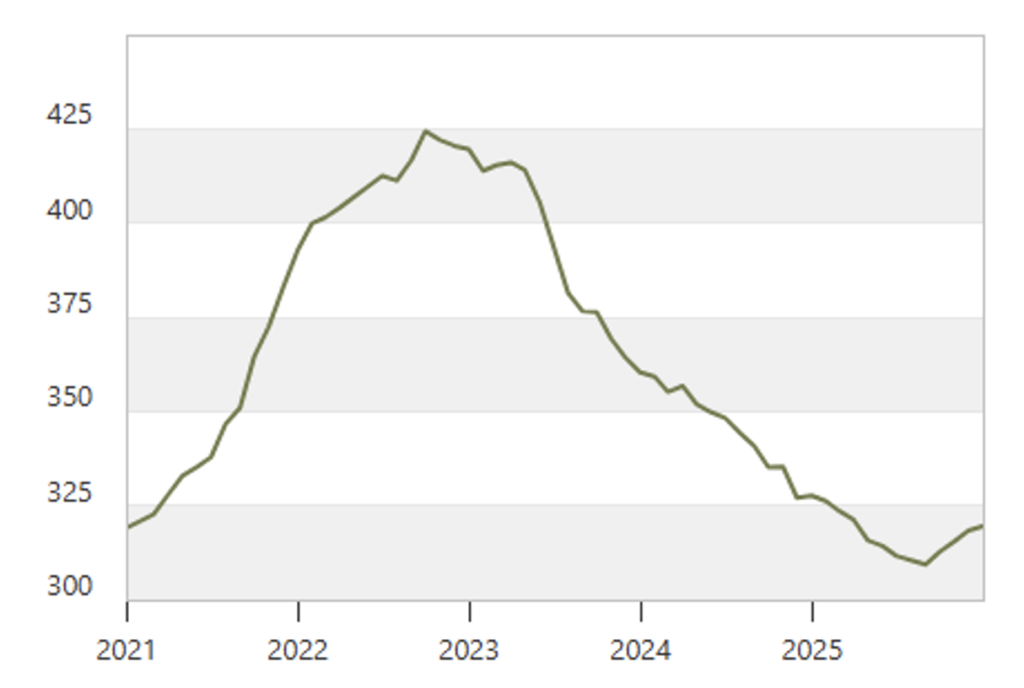

When Covid restrictions ended, the fine wine trade suffered a setback due to rising interest rates, concerns about the cost of living, and fears of a tariff war. Between the end of 2022 and the fall of 2025, fine wine prices fell by around 25%, according to the Liv-ex 100 index, which tracks the 100 most sought-after varieties (see Figure 1).

Figure 1. Liv-ex Fine Wine 100 Index from 2021 to present. It is the industry’s leading benchmark for tracking fine wine prices. It represents the price performance of 100 of the most sought-after fine wines on the secondary market.

Although prices have since recovered slightly, the pressure has been felt most acutely by wine merchants such as Oeno, which expanded rapidly during the boom years.

In June 2021, there were signs that Oeno might be able to turn the tide. It announced the launch of a new investment fund in fine wines and whiskeys based in Portugal. The goal was to initially raise €20 million with a minimum investment of €50,000, and in October, investors received new hope when an email arrived saying that Oeno was preparing for a “new chapter under new ownership and leadership.” The message said that Oeno Group was “set to become” a wholly owned subsidiary of Casa del Fuego Family Office & Trust, an international investment company that manages over $30 billion in assets.

This too was all smoke and mirrors. Oeno will probably have to go into administration: it appears that only 20% of the wine owned by investors is held in individual accounts that they can access. Many of the company’s investors are hoping that the City of London Police, which runs Report Fraud, will launch an investigation into Oeno: an update from the police is expected shortly.

In short, the situation appears to be as follows:

• The British company Oenofuture Limited — linked to the group — has been shut down by the authorities and investors are now unable to recover their money or the wines they purchased, nor do they have clear confirmation of the actual existence of the promised bottles.

• Hundreds of investors in several countries have reported being unable to access their wine or whiskey portfolios, with estimated losses exceeding several million euros in some countries alone (e.g., over €5 million in Portugal).

• Documents show that only a small portion of the wine purchased by investors was actually held in individual accounts; the rest appears to be in a single account managed directly by the company itself, creating major problems of traceability and ownership.

• In many cases, investors had not even physically seen the bottles they purchased, relying solely on virtual portfolios or internal documents.

That said, we believe it is useful to draw up a short guide with useful guidelines for investing in this type of alternative asset, with the caveat, of course, that this is not advice. Below, we will use the words “client” and “investor” interchangeably, referring to both private investors (individuals or companies) and collective investment vehicles, including specific instruments such as certificates (Actively Managed Certificates and Trackers).

Concept and nature of investing in fine wines

An investment in fine wine is considered an alternative investment in a tangible asset: it is not a financial security, but a real commodity that can increase in value over time due to scarcity of supply, growth in global demand, and the natural aging of wine.

In summary:

• The value depends on factors unrelated to traditional financial markets, such as the reputation of the winery, the quality of the vintage, global demand, and storage.

• The time horizon is medium to long term (typically 5+ years).

Purchase and ownership of bottles

Direct purchase from the real market

In the transparent model:

• The investor purchases specific bottles (potentially from auction houses, producers, en primeur markets, or platforms).

• These bottles are stored in specialized warehouses (often bonded or tax warehouses) to ensure preservation and tax benefits (exemption from VAT and excise duties until release).

This method requires:

• Clear documentation of ownership of the bottles in the customer’s name.

• Certificates of deposit issued by the warehouse.

• Traceability through reliable systems.

Model adopted by Oenofuture Limited (at the center of the scandal)

According to investigative sources:

• Investors never physically saw the bottles they purchased; the wines were selected by specialists on their behalf.

• The bottles had to be stored in warehouses such as London City Bond, which offered tax advantages.

• However, many of these bottles were not registered in individual accounts in the customer’s name, and some were apparently held in a single account controlled by the company.

• As a result, the certificates provided to investors were internal documents and not legal proof of ownership: this means that in the event of insolvency, actual ownership is uncertain and difficult to recover.

This type of model lacks asset segregation: i.e., client assets are not separated from the company’s assets. In the event of the operator’s bankruptcy or insolvency, there is no guarantee that these assets can be automatically returned to investors.

Role of custodians and traceability

Physical storage

In the proper market:

• Wine is stored in specialized warehouses with controlled temperature, humidity, security, and vibration-free conditions, preventing deterioration.

• The custodian issues certificates of ownership in the investor’s name or, in more advanced systems, uses blockchain/NFT to ensure traceability and authenticity.

Essential proof of ownership

One of the main lessons of the current scandal is that documentary proof of ownership of the bottles is essential. Without titles registered in the customer’s name, the investment becomes subordinate to the operator’s financial balance (in this specific case, Oeno).

Yield strategies and secondary market

Natural appreciation

The rarity and scarcity of quality wines lead to:

• Increased value over time due to growing demand and limited supply.

• Market indices such as the Liv-ex Fine Wine 1000 track price trends and show attractive average annual historical performance compared to traditional assets.

Secondary market sales

Investors can:

• Sell bottles through auctions, wine brokers, or specialized platforms.

• Obtain liquidity based on demand for that particular wine at a given time.

Key operational risks

The main risks, also highlighted by the scandal, include:

• Lack of segregation of assets: client assets not separated from those of the investment promoter.

• Inadequate documentation: internal certificates or documents that are not legally binding.

• Possible repeated sale of the same assets to different investors (risk of document fraud).

• Difficulty in physically accessing the assets: some investors have been unable to locate or verify the actual existence of their bottles.

Operational requirements for investors

In operational terms, an investment in fine wine should include:

• Guarantee of ownership registered to the customer with legally valid certificates.

• Storage in trust warehouses or segregated accounts.

• Transparent documentation with independent control of bottle custody.

• Clear policy on liquidation or sale on secondary markets.

The absence of these elements constitutes a substantial risk, as highlighted by the current scandal involving Oenofuture Limited.

Disclaimer

This post expresses the personal opinion of the Custodia Wealth Management staff who wrote it. It does not constitute investment advice or recommendations, personalized advice, and should not be considered an invitation to carry out transactions in financial instruments.