Let’s return to the topic of Switzerland and, in particular, the sector to which we belong: the financial market and its players.

In our opinion, a dual scenario is emerging that could pose a risk to the Swiss financial system, although we are well aware that where there is risk, there are also opportunities. Let us explain further.

On the one hand, the highly regarded Swiss financial sector is losing ground because stricter rules and consolidation in the sector are forcing smaller asset managers and private banks to close or merge.

According to records kept by the regulatory authority (FINMA), portfolio managers and wealth advisors, there were 1,570 authorized financial institutions last month, a sharp decline from the more than 2,000 that existed before the new rules came into full effect in 2022: the Financial Institutions Act (FIA) and the Financial Services Act (FSIA). The new regulations were intended to bring Switzerland’s fragmented asset management sector into line with global standards, introducing licensing for portfolio managers and trustees and extending supervision to small asset management companies for the first time. However, the short-term result was a significant increase in the costs and complexity of complying with the new regulatory framework, which had a particular impact on small managers.

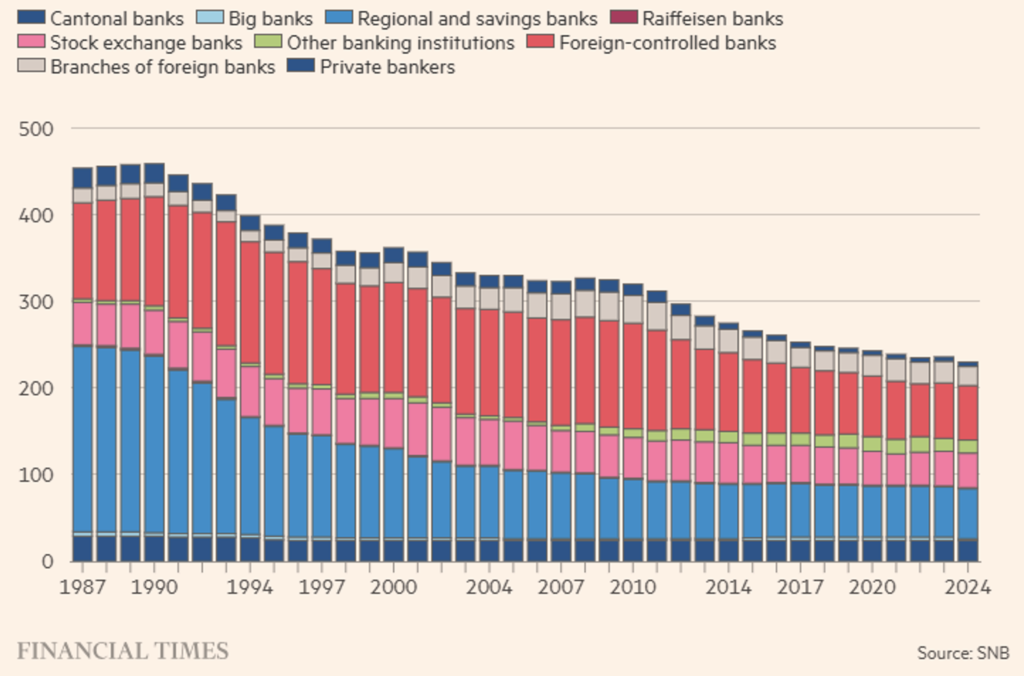

The number of private banks in Switzerland has also fallen from over 100 ten years ago to 82 today, according to data provided by KPMG, which predicts that this figure could fall below 70 by 2030. In general, all categories of banks have seen a decline in numbers in just over twenty years (see Figure 1). This is due to stricter regulation for small banks (less than CHF 10 billion in AUM), followed by an escalation triggered by the Credit Suisse case, which led to a rethinking of prudential supervision for systemic banks, namely UBS (see our insights of April 3, 2025, and September 15, 2025, which analyze the reform package known as Too Big To Fail).

Assets under management in Switzerland continued to grow, albeit at a slower pace than in emerging rival jurisdictions such as Singapore and Hong Kong. This was obviously not only due to the introduction of the new Swiss financial market regime, but also to the end of banking secrecy and the introduction of international tax transparency rules (such as FATCA).

On the financial market regulatory front, Switzerland has decided to make a U-turn and go against the grain of other countries such as the US (which is deregulating) and the UK, which has delayed the adoption of Basel III. There is another very specific financial area where Switzerland is changing its approach: the stablecoin sector. With the Helvetia project, the confederation seemed to be focusing on the introduction of the digital franc, but now it seems to have changed course here too.

The government has launched a public consultation to allow the issuance of stablecoins in the country by proposing new license categories for “payment instrument institutions” and “cryptocurrency institutions,” which would bring stablecoin issuers under Swiss financial legislation.

We are, of course, talking about stablecoins pegged (algorithmic ones will not be allowed) to various assets and not just to the Swiss franc, although it is conceivable that the new regulatory framework will encourage the issuance of a stablecoin pegged to one of the world’s most stable fiat currencies because it is guaranteed by a solid country system and would be under the direct supervision of FINMA.

Figure 1. Trend in the number of Swiss banking players by year and category.

A franc-based stablecoin could also attract users seeking alternatives to the dominance of the dollar in cryptocurrency payments. The reliability of the franc could attract investors who want digital liquidity without being tied to US monetary policy or the reputational baggage of offshore issuers. The Swiss proposal draws clear lines: coins issued in the country will require a license with guarantee requirements (presence and level of reserves to guarantee the “peg”) and transparency; foreign coins simply traded in the country will be treated as cryptocurrencies, not as legal payment tokens. Offshore issuers will not be forced to transfer or duplicate reserves, while coins issued in Switzerland will remain strictly controlled by FINMA.

The consultation—open until February, with legislation unlikely to be enacted before the end of 2026—shows delays compared to other competing countries such as Singapore, Hong Kong (them again?), and Dubai, eager to court global digital asset companies. Also in the pipeline is the removal of the 100 million Swiss franc limit on the amount of customer money that authorized fintechs can hold, a change designed to allow such institutions to “exploit economies of scale.” In essence, this is a significant signal that new digital currency providers are set to grow, even if it means more competition for banks.

And this is where the devil comes in. The more convincing the new institutional framework for Swiss stablecoins becomes, the greater the threat to the system that will generate them. In a world where digital francs can circulate globally through simple transactions made with special apps, the need for a Swiss bank account – or even a Swiss intermediary – diminishes. Why park money in the Alpine country when you can hold it in the same currency, from your own wallet? The risk for Swiss banks is not the failure of stablecoins (not least because the legislation aims to guarantee their soundness), but their excessive functioning.

Let’s put the facts in order: increasingly strict and stringent legislation and regulations for financial operators, whether banks or asset managers, are being supplemented or integrated by legislation and regulations in favor of private issuers of digital currency, which clearly constitutes a prelude to the cryptographic digitization of all securities (the tokenization of stocks, bonds, and derivatives), which would clearly benefit from the adoption and circulation of on-chain currency.

One of two things is true: either the Swiss authorities are a little confused and do not know which direction to take, copying their “classmates’ exams,” or the longer time frame they have taken is the basis on which to build a more modern financial sector, with very clear signals to current operators to start thinking about the change that is being outlined.

Disclaimer

This post expresses the personal opinion of the Custodia Wealth Management staff who wrote it. It is not investment advice or personalized advice and should not be considered an invitation to carry out transactions on financial instruments.