“What do you say Jacob, will the next bubble be green?” This is one of the final lines of the movie Wall Street – Money Never Sleeps. Since the last major financial crisis of 2008-2011 many have tried to grapple with the prediction of the next bubble, and as always no one succeeds in this improbable task. This has to do with the fact that one cannot – on a scientific level – give a precise definition of a speculative bubble and consequently of the “bursting” of the bubble itself. If you can’t define it, you can’t measure it either, of course. Neoclassical economists who assume the absolute rationality of economic agents as a premise for their choices describe financial bubbles as a “violation” of the basic assumption of perfect rationality. At the opposite end of the spectrum, however, we find proponents of behavioral finance who somehow argue that bubbles are physiological because investors are affected by a series of cognitive distortions that lead to exaggerated assessments of the value of financial assets (not just stocks) that result in marked price rises followed by a sudden collapse of prices.

Eventually when bubbles form, everyone benefits, not just insiders. Even government authorities and regulators see no cause for concern unless inflation soars: and that is usually never the case. Otherwise when things are going well on average the main macroeconomic indicators (unemployment, budget deficits, tax revenues) show healthy or at least not worrying metrics and from a political point of view this increases the consensus of the political forces in government: so why worry? Problems arise when for some reason financial asset prices collapse and looking at the situation in retrospect one realizes that certain valuations were abnormal if not when absurd. But what triggers a price collapse? Probably too high a percentage of consumer credit that is not useful for GDP growth: when it becomes unsustainable, defaults occur and a snowball effect begins. It certainly happened during the sub-prime crisis, but also during the Internet bubble that burst at the beginning of the new millennium when asset-less and hugely overvalued and indebted companies could not meet the debt themselves.

Now we ask why green investments should lead to a speculative bubble. There are basically two facts that could have fueled inflated valuations prodromal to a sudden collapse:

1. Green and energy transition investments.

2. The costs of environmental disasters (hurricanes, floods, heat waves, etc.).

The first case in point originates from investments in fossil fuel-related technologies (and related debt) that could become problematic the moment the guidelines related to decarbonization become-at the behest of states-increasingly stringent undermining the value of fossil fuel investments, triggering precisely a possible crisis originating from the “carbon” sector.

The second case, on the other hand, is directly related to the value of real estate in areas subject to “climate shock,” and in particular the cost of insurance. There is no single scenario that spells out exactly how property insurance costs could lead to climate-induced financial upheaval, so let us try to outline one, the one we think is most likely. From an inescapably global perspective, it begins with premiums rising for properties located in hazard-prone areas until insurers withdraw from these abandoned areas because of the unprofitability of offering insurance coverage. Homeowners will, in the first instance, face soaring premiums and the inability to renew insurance coverage in the second instance, while insurers will face a relentless wave of fires, storms, and hurricanes. Governments will try to fill the gaps with insurance plans of last resort. But these plans usually cost more and cover less, raising a chilling new reality for thousands of homeowners. The value of the family home, which had been rising year after year, will instead begin to decline. The contagion will spread because insurance will be required to obtain a mortgage, so as housing coverage weakens, we will also see a restriction of bank credit, if not even its elimination. In city after city, people will find themselves living in houses that will be worth less than they paid for them. Each monthly mortgage payment will seem a bit like exchanging good money for bad.

In an eerie reminder of the financial turmoil of the past, mortgage defaults will begin to rise, along with foreclosures and – in the United States – credit card delinquencies. But this time will be different. Unlike other financial disasters, this time the root cause will not be financial, but physical, and it is unclear how it will end.

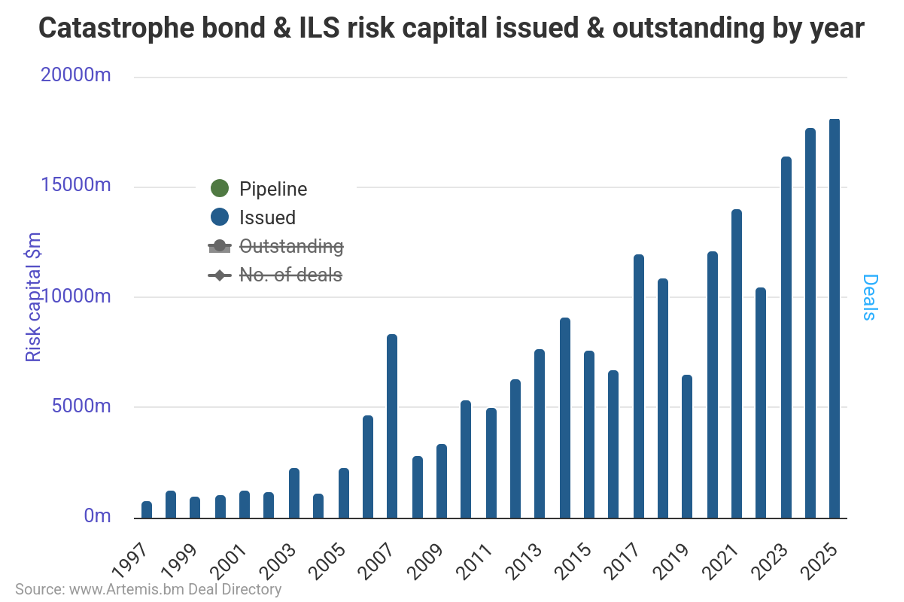

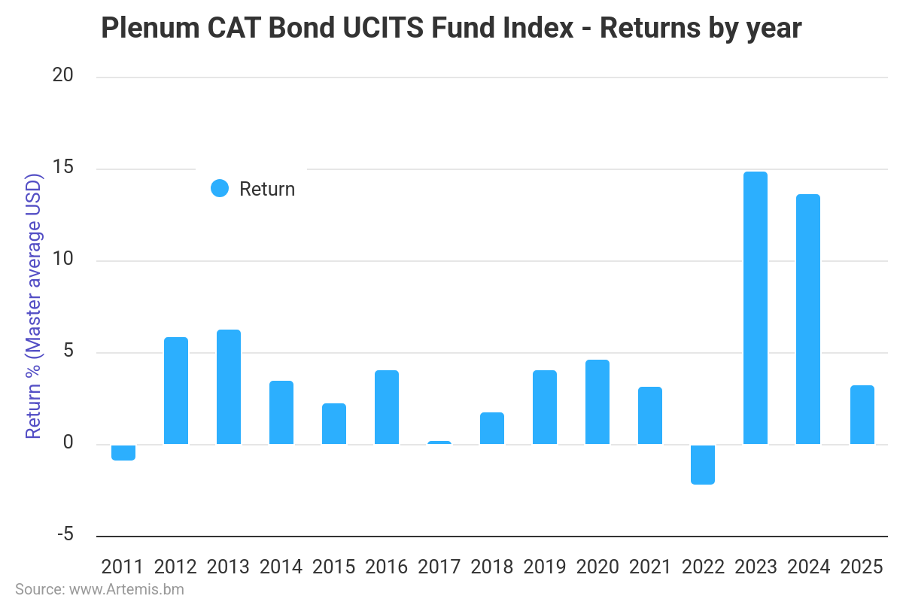

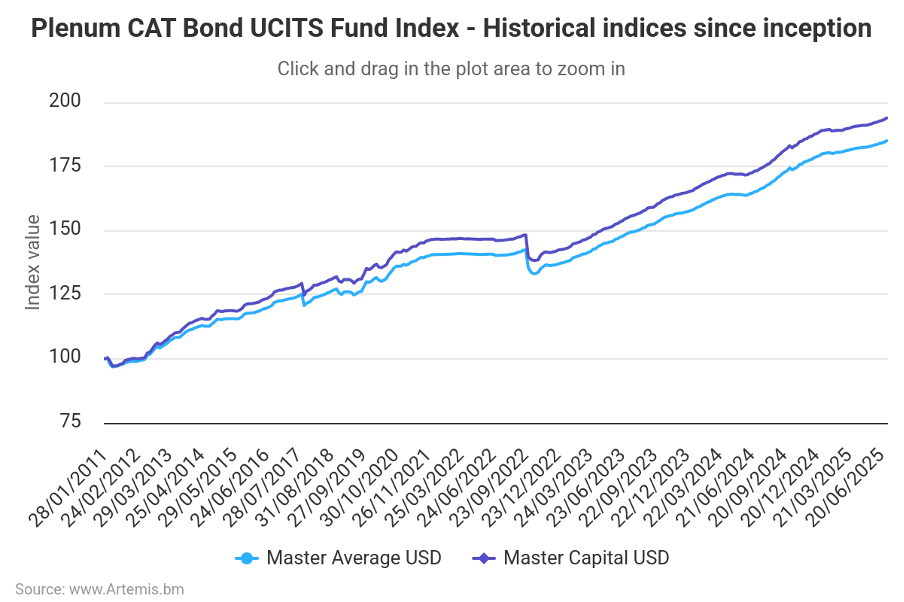

Corroborating these scenarios are data on the issuances of CAT bonds a.k.a. catastrophe bonds (see Figure 1): a form of reinsurance, through which insurers grant payments to investors to assume some of the risk from events such as extreme weather. If a catastrophe occurs, bondholders can lose their money; otherwise they benefit from very attractive returns compared to traditional bonds and especially uncorrelated with financial asset returns (see Figures 2a and 2b). These bonds are the component of a basket of insured risks (excluding life risk of individuals) that is sold to investors as a financial product called ILS (Insurance-Linked Securities). We will cover these products in one or more dedicated posts. For the time being, we would like to draw attention to the fact that similar to CDOs (Collateralized Debt Obligation) that packaged mortgages of varying quality (including junk, the infamous “sub-prime”) by transferring the default risk onto the investor, with ILS we are witnessing a transfer of catastrophe risk; but the substance does not change: we are talking about debt that does not produce GDP and therefore a harbinger of functioning as a detonator of a financial crisis.

Figure 2a. Annual returns of CAT Bonds constituting the underlying index of a UCITS fund.

Figure 2b. Historical performance of the underlying CAT Bond index of a UCITS fund.

We also point out that the two cases are not necessarily disconnected. Unfortunately, they may constitute the two self-feeding components of a single crisis spiral: extreme events will push governments to increasingly stringent and strict transition policies, which in turn will exacerbate transition risks.

As we tried to argue in our incipit, it is difficult to tell whether or not we are in a financial bubble of whatever nature. In our view, the climate change scenario that is inextricably linked to the ecological transition has merit. Certainly, for an analysis to make any sense, we need to clear the field of mindless denialism that is now permeating U.S. institutions (from the Federal Insurance Office to the Fed) and will affect their choices and positioning in the near future.

Disclaimer

This post expresses the personal opinion of the Custody Wealth Management employees who wrote it. It is not investment advice or recommendations, personalized advice and should not be considered as an invitation to conduct transactions in financial instruments.