Despite the recent jaw-dropping performance of the yellow metal, we want to try to understand why gold might continue to rise, at least for one more year. We provided some data on the gold market in our in-depth report on May 9. In the present report we want to try to understand the trends at least in the short term of the price of the quintessential precious metal.

The incontrovertible fact is that central banks have accumulated significant gold reserves since the Russian invasion against Ukraine bringing global storage to about 37,000 tons i.e., slightly less than that recorded in 1965 at the height of the Bretton Woods regime (source: European Central Bank). Central bank reserves now see gold as the second largest allocation after the U.S. dollar surpassing, albeit slightly, that in euros. This accumulation is probably mainly responsible for the rise in the price of gold (doubled in one year).

Undoubtedly underlying these choices is the geopolitical factor brought about by the worrying open war fronts that have led to a growing distrust of the greenback in favor of the yellow metal.

Apart from the obvious disadvantages of the “gold” asset, which are attributable to the fact that it does not produce interest, but – on the contrary – costs (storage and transport), the advantages it offers far outweigh the drawbacks: liquidity, the lack of counterparty and insolvency risk (when one holds it oneself, of course), protection from inflation (less and less relevant, to tell the truth), but above all – increasingly important – protection from international sanctions such as the freezing of financial assets or exclusion from international payment systems. This would also explain why among the countries that have done the most in the past year to increase their gold reserves are those that gravitate in the Russian orbit, such as India and China (see the graph on the left where the green bars illustrate the increase in tonnes of gold accumulated during 2024).

If one adds to this situation decidedly worrying US policies (such as the infamous tariffs), one cannot be surprised by the decline in confidence in the dollar in favour of a financial asset that has always been the basis of international currency systems.

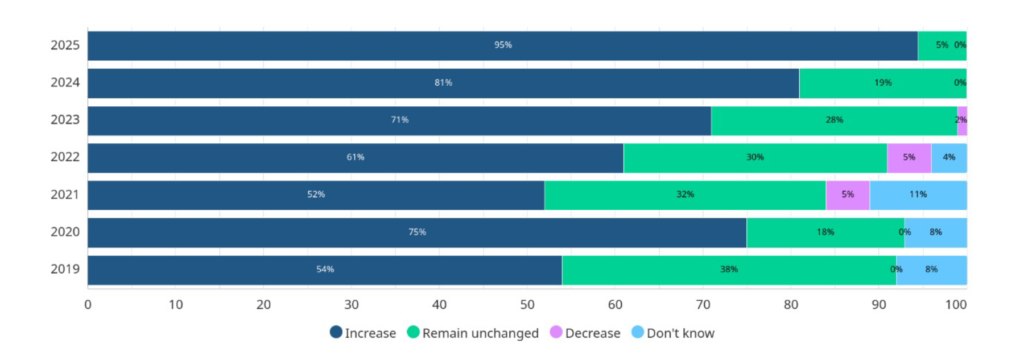

In a recent World Gold Council (WGC) survey, 95 per cent of respondents predicted an increase in global central bank gold reserves over the next 12 months (see Figure 1) and a 75% assumes a decrease in the dollar holdings of central banks in the next five years. To which new store of value remains to be seen (because there are also cryptocurrencies, and Bitcoin in particular – at least to date).

Figure 1. How do you expect the gold reserves of the world’s central banks to change over the next 12 months? WGC survey.

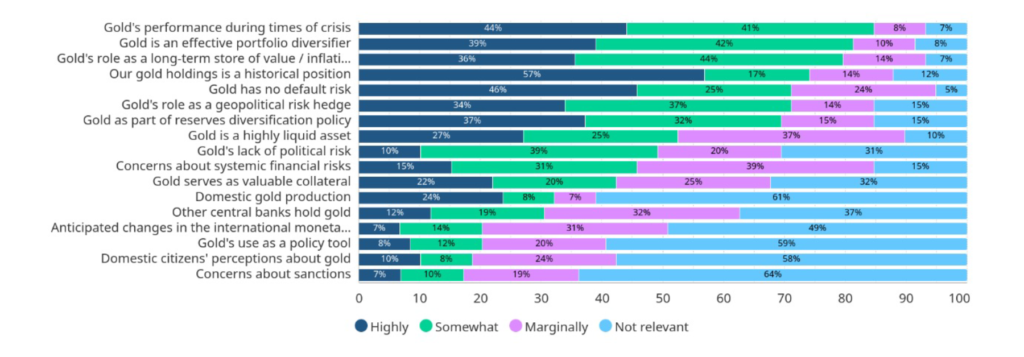

Among the most important reasons for holding gold, the WGC survey itself reports the following answers (see Figure 2):

Figure 2. How important are the following factors in your organisation’s decision to hold gold? WGC Survey.

Finally, we see a signal that – in our opinion – is unmistakable: the call on countries that are important, both from an economic point of view and in terms of gold reserves held, to repatriate gold held abroad, particularly in the United States where New York is, together with London, the world’s largest centre for the storage and exchange of precious metals. We are talking about countries such as Germany and Italy, which are respectively the second and third largest holders of gold reserves in the world. Accumulated over decades, the storage of gold by the monetary authorities of these two countries (but it is also true for the others) has been diversified in different locations precisely to mitigate the risk of concentration that could facilitate embezzlement or plundering practices following, for example, conflicts: during the Cold War, the US vault proved to be the safest and most reliable in the world. A few months of an “extravagant” policy of the star and stripes executive have undermined its standing and reputation as a “vault” (see Figures 3 and 4). But on this front, we are waiting for the transfers to actually occur before drawing conclusions with any foundation.

Figure 3. Gold reserves (metric tonnes) of the world’s major central banks.

Figure 4. Gold reserves (metric tonnes) of the Bundesbank differentiated by storage site.

Disclaimer

This post expresses the personal opinion of the employees of Custodia Wealth Management who wrote it. It is not investment advice or recommendation, personalised advice and should not be regarded as an invitation to trade in financial instruments.