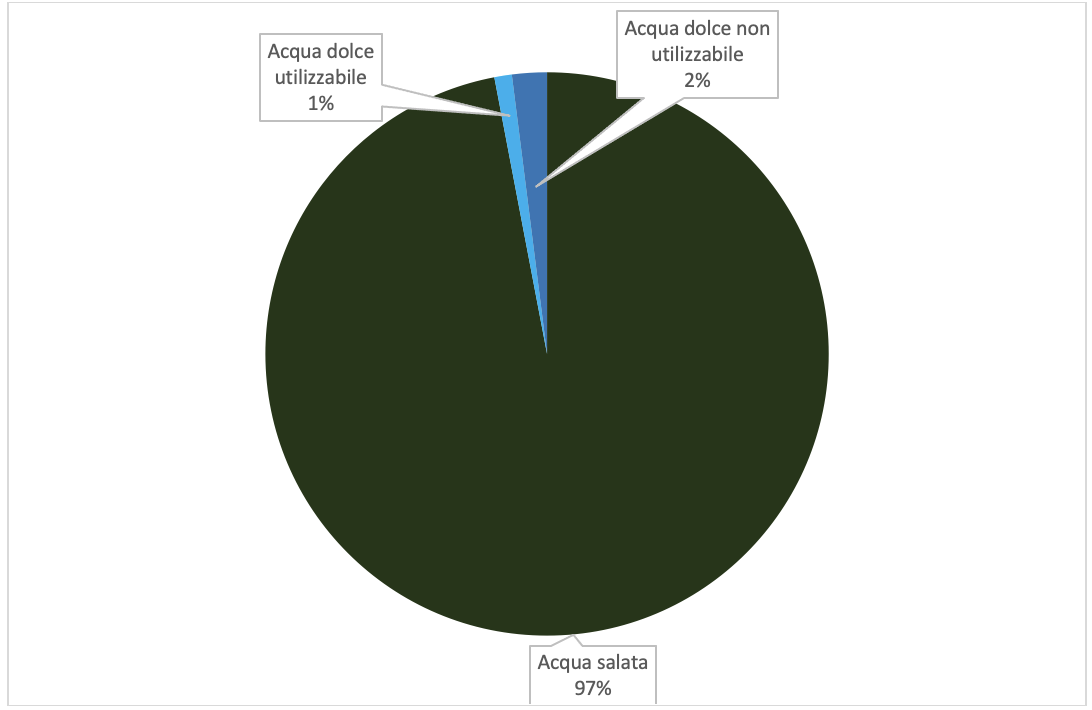

Together with electricity, water can be considered the most important commodity we have: and unfortunately we have very little of it. Approximately 70% of the earth’s surface is covered by water, but over 97% is salt water. Salt water cannot be used for drinking, irrigating crops or most industrial uses. Of the remaining 3% of the world’s water resources, only about 1% is readily available for human consumption.

Water and electricity are not only important commodities for production, but for life itself. However, the very use of water as a commodity for industrial and agricultural purposes has led to a worrying shortage of this precious resource. China, Egypt, India, Israel, Pakistan, Mexico, most of Africa and the United States (Arizona, New Mexico, California and West Texas) are areas that have experienced a shortage of usable fresh water.

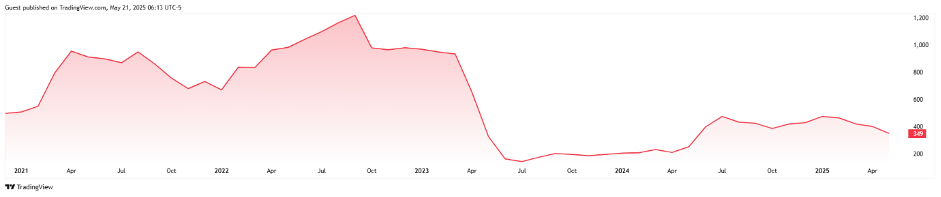

Pollution is another cause of water scarcity because dirty water reserves further limit the amount of fresh water available for human use. So if the commodity we are talking about is usable freshwater reserves that are only 1% of the entire stock of water on the planet, we can ask ourselves whether it would not be worth reusing this scarce water: and reused water would then become an even more valuable commodity. However, to open up a market like this – entirely new and innovative – we would need incentive instruments similar to the green certificates (declined in their various forms, from carbon credits to GO/RECS) used to clean the air of greenhouse gases. We are thinking of a kind of blue certificates that would reward those who do not waste or reuse fresh water. Similar to green certificates there can be both voluntary and mandatory markets. However, these kinds of instruments are not yet available on a large scale (with a few exceptions with interesting and innovative solutions). The only structured way – that at least we know of – to invest in water as a commodity is currently the futures on the Nasdaq Veles California Water Index (see chart below).

The index (NQH2O) is calculated by WestWater Research through Waterlitix™, the largest and most comprehensive source of prices for water transactions in California, and seeks – the first case in the world – to track the spot price of water in the Californian state.

Its main features are:

- – value expressed in US dollars per acre-foot ($/AF) at source, excluding transportation costs and losses (one AF is equivalent to 325,851 gallons, or approximately 1233 cubic metres of water);

- – is calculated and disseminated once a week after the close of business on Wednesdays, representing all data up to the end of the previous week;

- – represents the volume-weighted average of water prices and shows the current level of water prices in California as determined by the water rights transactions of five water markets:

- – Surface water

- – Central Basin

- – Chino Basin

- – Main Basin

- – Mojave Basin – Upper Subarea

- – reflects changes in the relative scarcity of water in California;

- – WestWater is the exclusive data provider that powers the Index.

WestWater’s value is expressed by its proprietary database of water rights sales and leases over the past two decades. With over 30,000 archived transactions,

Waterlitix™ maintains detailed information on prices, quantities and other transaction terms, verified through interviews with interested parties and confirmed by filing documents.

The future, which also has this index as its underlying, is issued by NASDAQ at quarterly expiry dates and quotes 10 index points per contract with cash settlement. This investment solution, although attractive, has its drawbacks. Usually a commodity future requires high levels of standardisation, e.g. on the characteristics of the underlying, which often has a ‘physical’ spot market. In the case of water, this standardisation risks not presenting the appropriate characteristics for a global future because an acro-foot has different specificities depending on the area where it is produced and used. There is therefore a risk of producing different futures depending on the zone where the water ‘resides’, which is not really a desirable characteristic for this kind of instrument. This is why we believe that investing in water as a commodity is best done with the certificate model.

Apart from this instrument, it is very complex to invest in water as a commodity. Today, there are mainly both passive and active funds that invest in shares of listed companies involved in various water-related issues. They are mainly divided into two categories: water services and infrastructure and water equipment and materials. Within these categories we find companies involved in providing distribution services, filtration services and flow technologies among the main ones. More specifically, companies to invest in to profit from water-related activities include beverage suppliers, utilities, water treatment/conservation and purification companies, and equipment manufacturers, such as those supplying pumps, valves and desalination units. Specifically, according to a 2018 United Nations study, 177 countries rely on desalination for at least part of their freshwater needs. Companies that manufacture equipment and offer services in this area are obvious candidates to enter the portfolio of these funds.

Apart from investment in companies specialising in the treatment of this vital material and related services, we are still in an immature market as far as water as a commodity is concerned. We can therefore expect a significant development in the coming years on this front also because – to go back to one of our previous posts – we are aware of investment opportunities related to royalties on water signalling that we are moving in various directions to make this investment theme a non-negligible opportunity for the years to come that we hope will succeed in combining the reasons of profit with those of sustainability.

Disclaimer

This post expresses the personal opinion of the employees of Custodia Wealth Management who have written it. It does not constitute investment advice or recommendations, nor should it be considered as an invitation to trade in financial instruments.