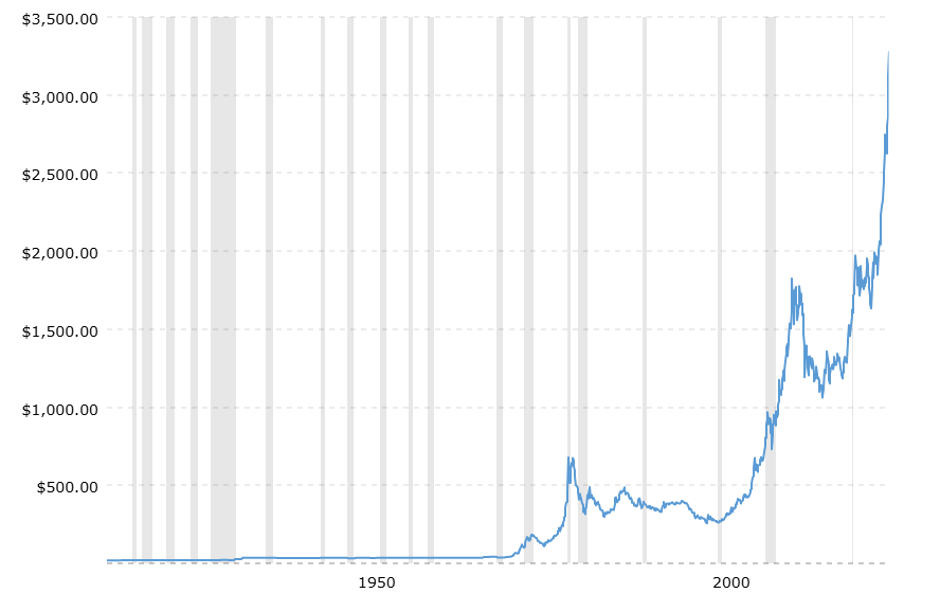

For at least a year now, gold has become a major investment theme in the world. The unbelievable increase in its price (see Figure 1) testifies to a real rush to grab gold either through direct purchases of physical gold or through financial instruments that peg their price to that of the underlying physical gold (such as ETCs).

![]()

Figure 1. Gold spot price. Monthly data from January 1915 to April 2025 (source: www.macrotrends.net)

Figure 1. Gold spot price. Monthly data from January 1915 to April 2025 (source: www.macrotrends.net)

One may ask why there has been this unbridled ‘gold rush’ and to give an answer we have to look at the inflation-adjusted price of the yellow metal (see Figure 2). Both of these graphs highlight with light grey vertical bars the time interval of some financial and/or economic crisis. In Figure 2, an inflation-adjusted price peak at the beginning of the 1980s (around 2800), the period of the oil crisis accompanied by a marked rise in the price index (and not only in consumer prices), immediately stands out. Inflationary pressures characterised by the war in Ukraine thus explain part of the all-time high reached by the gold price in this first quarter, which testifies to the extent to which gold is an asset that protects against inflation even in the medium term.

Another motivation behind this year’s demand probably lies in the investment in a safe haven asset. But why is gold considered the undisputed king of safe haven assets? Let’s say that a first banal answer stems from the fact that other safe haven assets such as the US Treasury or the Swiss franc present criticalities: the former linked to the enormous indebtedness of the United States, the latter to the solidity of a small economy that could soon be put to the test in the ‘threatened’ war on tariffs. But of course it makes no sense to limit oneself to a comparison with substitutes alone to give an exhaustive answer.

Indeed, physical gold possesses certain characteristics that make it particularly suitable as a safe haven asset. First of all, the fact that it is a material that perishes very little over time (a kilo of gold produced today will also be a kilo in a hundred years’ time) and is therefore particularly suitable as a store of value. Moreover, it has very standardised characteristics (a gram of gold differs from another gram of gold only in purity) and thus makes it suitable to serve as currency.

Figure 2. Gold spot price. Monthly data from January 1915 to April 2025. Spot prices are adjusted for inflation using monthly CPI data (source: www.macrotrends.net).

Figure 2. Gold spot price. Monthly data from January 1915 to April 2025. Spot prices are adjusted for inflation using monthly CPI data (source: www.macrotrends.net).

These characteristics – to tell the truth – are shared with many precious metals. But gold also has a history that makes it more suitable as a safe haven asset than others. Until 1971, it was the lynchpin of the Bretton Woods system created in 1944 to facilitate international trade by linking the issuance of money (and thus also currency exchange rates) to the gold reserves held by the central banks of the countries that signed the agreement. For example, the Federal Reserve could issue $35 for every troy ounce held in storage. Trade imbalances were settled in gold: thus the country with a trade surplus reset its surplus to zero by buying gold from the central banks of the deficit countries. Even after this standard was abandoned and the transition to a floating exchange rate system, gold continued to play a key role in international transactions. The Asian crisis of 1997 had led to such a devaluation of the South Korean won by more than 100% that it was impossible for the country to repay its foreign debt. Solvency was only possible thanks to domestic gold collected by the government and converted into dollars.

This history should explain well the conformation of the gold supply, which is mainly composed of reserves accumulated over time and only to a small extent of new production. So the price will only rarely be affected by shocks that depend on mining dynamics as is the case with other metals or other commodities.

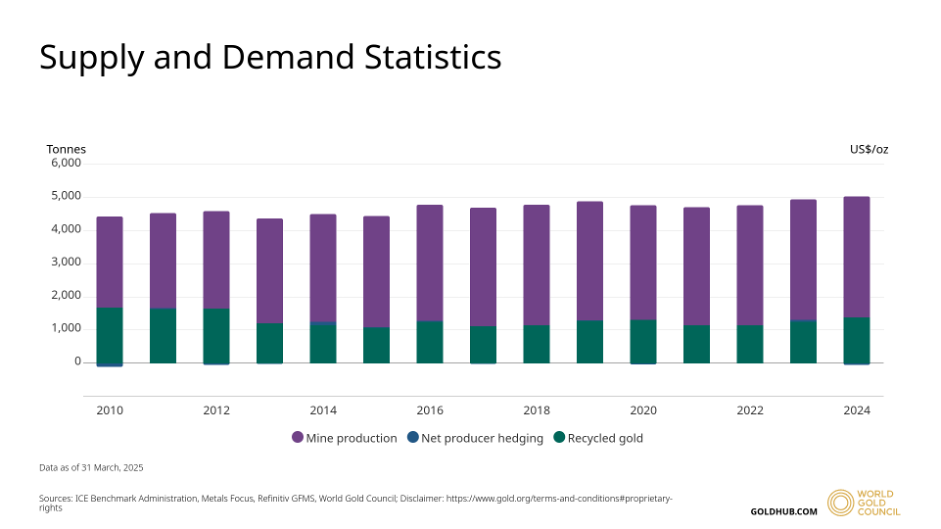

Figures 3 and 4 are very comprehensive because they clearly show that new gold mining in the last 15 years between 2000 and 4000 tonnes per year constitutes only 1%-2% of the entire gold stock.

| Total above-ground stock (end-2024): 216,265 tonnes

|

*End-2024 estimates from Metals Focus. Reserves are the portion of an ore deposit that can be economically extracted. For an ore deposit to be considered a reserve, numerous factors will have been assessed e.g. geological, mining, processing, marketing, economic and ESG. Only once all of these have been taken into consideration and the ore is still economically viable will it be considered a reserve. Projects that have reached feasibility stage are likely to fall into this category. There are two types, proven and probable. Resources are the portion of a deposit in which companies have less geological knowledge and confidence in, i.e. less drilling data and only simple economic modelling applied to it, or in some instances no economic modelling at all – it’s a broad category ranging from inferred, indicated to measured. Estimates for reserves and resources can vary, for example reserves are currently estimated to be ~64,000t by the US Geological Survey.Figure 3. Source: Metals Focus, Refinitiv GFMS, World Gold Council (WGC) | |

Figure 4. Gold supply since 2010. Annual data. Source: WGC

Figure 4. Gold supply since 2010. Annual data. Source: WGC

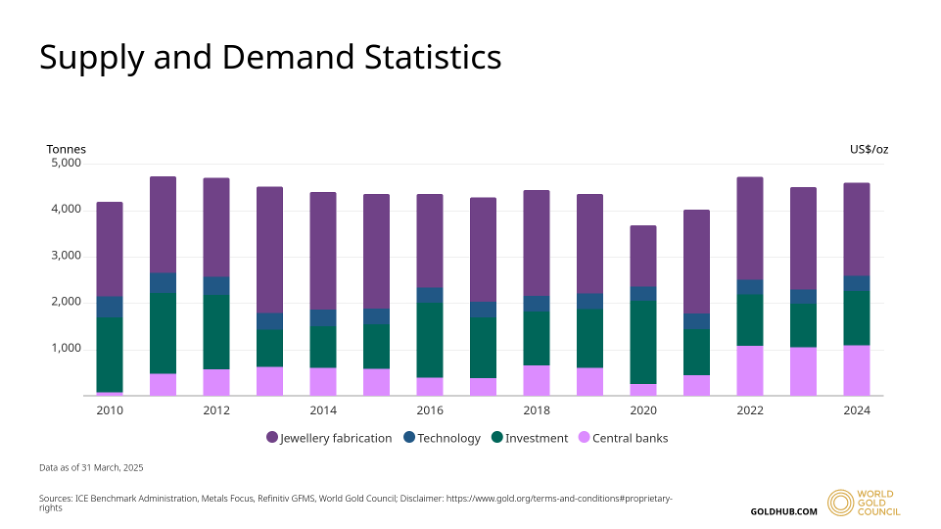

On the other hand, the demand for gold is largely driven by the luxury industry (jewellery in particular) and to an increasing extent by investments and central bank reserves (see Figure 5).

Figure 5. Gold demand since 2010. Annual data. Source: WGC

Figure 5. Gold demand since 2010. Annual data. Source: WGC

Note that the surge in the gold price starts in 2022 when central banks have intervened heavily in buying, at least compared to the previous 10 years. Will this trend continue in 2025? Hard to say. As always when we find ourselves in unexplored price ranges characterised by absolute highs to launch into predictions is always a difficult task.

Instead, we prefer to point out that there is another substitute appearing on the horizon, which in the narrative of recent years is equivalent to a kind of gold, albeit in ‘digital’ form: bitcoin. If we think that the characteristics listed above are decisive in considering gold the safe haven asset par excellence, we can ask ourselves and verify whether ‘digital gold’ also has – in whole or at least in part – these characteristics.

We note at the outset that the history of bitcoin is obviously much shorter than that of physical gold, having been born in 2010, yet there are some interesting similarities. We have said that physical gold does not perish; similarly bitcoin, or rather the blockchain that holds it (or rather it would be correct to say, where bitcoin is generated and ‘lives’), has reached such a spread that it seems impossible to destroy and certainly very difficult to attack. Creating a bitcoin substitute means replicating a number of nodes (currently around 22,000. For a detailed mapping see Coin Dance | Bitcoin Nodes Summary bearing in mind that bitcoin is a permissionless chain) and of users greater than that of bitcoin itself: an unthinkable investment because consensus algorithms, even the cheaper Proof-of-Work ones, still require a high investment to replicate the network effect of bitcoin.

Moreover, the stock of bitcoins created to date (see Figure 6) is enormously higher than the new production (currently estimated at 164,250 bitcoins in one year) when the stock consists of almost 20 million BTC. And new production will obviously tend to run out because the reward for miners (currently set at BTC 3,125) is halved for every 210,000 blocks created.

Figure 6. Historical trend of the cumulative number of mined bitcoins since its launch. Source: blockchain.com

Figure 6. Historical trend of the cumulative number of mined bitcoins since its launch. Source: blockchain.com

Obviously in terms of demand we cannot compare it to physical gold because bitcoin cannot be used by the luxury or even the technology industry. However, this demand can be replaced by services such as means of payment: and in this bitcoin is certainly not the best digital currency for payments, especially small ones, while it could absolutely compare to gold as an investment asset (think of the tracker industry buying it or corporate treasuries: see Bitcoin Treasuries | 91 Companies Holding (Public/Priv)), but especially the recent interest shown by central banks in creating bitcoin reserves. Moreover, bitcoin does not benefit from the possibility of issuing smart contracts and thus enjoys a high degree of standardisation in this respect.

This quick examination therefore leads us to consider the narrative in terms of ‘digital gold’ sufficiently well-founded to start considering bitcoin as an investment issue comparable to gold and thus a safe haven asset. It could be argued that its price is too volatile for this role. However, we would point out that gold also exhibits non-negligible volatility profiles and that volatility can always be controlled with a well-considered allocation. The annualised volatility calculated from 2010 to date is about 15% for gold and 150% for bitcoin, so it is a matter of allocating a tenth of a bitcoin for every point of physical gold (crude reasoning because we ignore correlation). And again one could argue that bitcoin is liquid while physical gold is not. Here again, however, it should be noted that physical gold is traded on the London Metal Exchange with two daily fixings. But of course if a transaction of physical gold involves transportation, then yes we have a big difference with digital gold which allows for large transfers of value with simple clicks assigning to the buyer’s addresses and deleting them from the seller’s. However, these objections do not seem strong enough for us not to seriously start thinking about digital gold as an alternative safe haven asset.

Disclaimer

This post expresses the personal opinion of the employees of Custodia Wealth Management who wrote it. It does not constitute investment advice or recommendations, nor should it be considered as an invitation to trade in financial instruments.