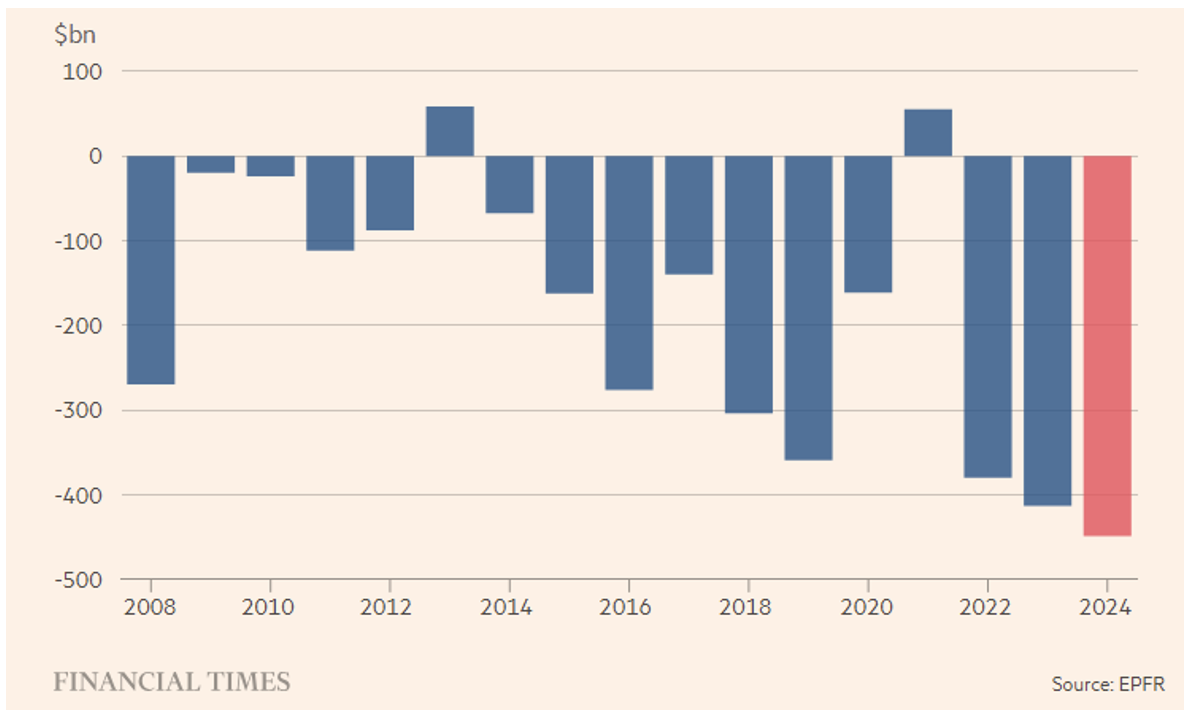

Today’s FT reports an article that neither surprises nor amazes, except for the fact that it highlights a new record—and usually, a new record is always noteworthy. We are referring to the capital outflow from the active fund (or mutual fund) industry, which focuses on stock picking, totaling $450 billion this year.

Who captured part of this liquidity? Obviously, the passive fund industry, first and foremost. The article focuses on the generational gap: active funds will disappear with the generational shift, as younger investors are more familiar with index trackers compared to older ones. To follow this trend, many firms are successfully packaging their active strategies into containers typically designed for passive strategies, such as ETFs.

To us, this seems like a contradiction or, if you prefer, mere window dressing. Let’s not forget that ETFs are traded on an exchange and subject to intraday trading. This allows arbitrageurs to eliminate any discrepancies between an ETF’s price and the value of its portfolio. This benefit would be desirable for active ETFs as well, but it requires total transparency (even in real-time) of the portfolio, making the manager’s alpha fully replicable. To prevent this, the SEC has allowed active ETFs to be less transparent than their passive “cousins.” In addition to reduced transparency, active ETFs carry higher management costs. Even assuming that performance fees (usually applied when generating alpha) are not charged, management fees are significantly higher than those of passive ETFs. But then, what differentiates them from a standard active fund? The stock market listing? Well, that can be done for active funds too!

Finally, a more theoretical consideration. Trackers have thrived on a simple premise: over the long term, (equity) markets are efficient, making it impossible to beat them through stock picking. Therefore, it is better to build a well-diversified portfolio to eliminate systematic risk and control idiosyncratic risk. And if a portfolio manager is truly skilled at consistently beating the benchmark over the medium/long term, they would be an excellent candidate to manage a long/short equity hedge fund. If all this holds true, why should an active ETF outperform the benchmark? And why should it defy the “law” of market efficiency?

To us, active ETFs do not seem like a major innovation. On the contrary, their underlying potential to reduce active management fees risks devaluing this activity, contributing to its implosion. If markets were genuinely efficient, any form of active management would be meaningless.

Instead, we highlight a new perspective emerging in the United States, which we hope will also spread to Europe in the medium term: direct indexing. This, we genuinely consider an innovation! In simple terms, it involves building your own index tracker “in-house,” implementing it directly in your Personal Account. But how is this possible? Transaction costs, replication complexity, and rebalancing within indices with many components—just to name a few challenges—undoubtedly make investing in passive funds more efficient.

The breakthrough is that many brokers can now offer electronic trading of liquid stocks at zero cost, along with the ability to acquire fractional shares. This allows for perfect replication of any index, even for small portfolios. Additionally, free software can now calculate the real-time percentage weight of each index component and offer automated, tracking error-minimizing investments and rebalancing. As a result, investors can create their own index tracker. Not only that! They can also customize it, for example, by underweighting some sectors (or stocks) and overweighting others. This way, they can even generate alpha “in-house.” True in theory, but in practice, it requires skill.

Disclaimer: This article expresses the personal opinion of Custodia Wealth Management collaborators who wrote it. It is not investment advice, personalized consulting, or an invitation to trade financial instruments.