Last Friday was definitely a black Friday for precious metals. Here are a couple of figures:

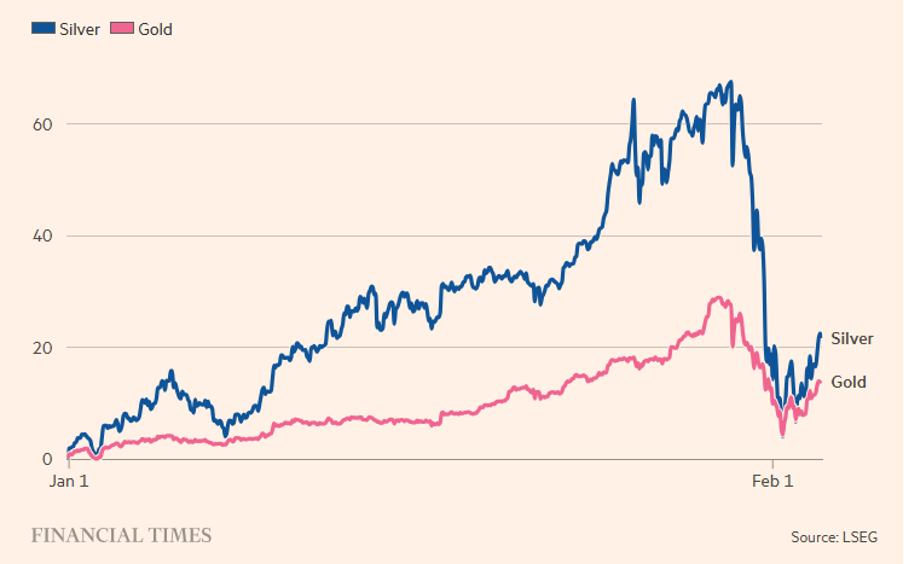

Silver: -30% from its peak in a few days (typical meme-stock drawdown)

Gold: -15/16%, a more moderate but significant movement for a safe-haven asset

Platinum: recorded a decline of about 18% on a daily basis during Friday’s sell-off, following the general decline in precious metals.

Palladium: lost over 7% on the same day, reflecting the downward movement related to the previous strong rally.

Figure 1. Silver and gold have lost most of their gains this year, as shown by the change in spot price (%) since the beginning of the year.

This has had knock-on effects on the US and Chinese stock markets due to the increase in margins required by exchanges to trade precious metal futures and, of course, a collapse in mining stocks, which have experienced negative amplification (β>1) relative to the metal.

In our view, this is a massive profit-taking exercise. We note that market dynamics have shifted from a parabolic rally to forced deleveraging, particularly in silver, which is characterised by strong retail participation, extensive use of leverage (leveraged ETFs, futures) and concentration in a relatively shallow market (especially silver).

The bullish movement was fuelled by geopolitical fears, US fiscal risk and doubts about the independence of the Federal Reserve; on Friday, it quickly turned into a phase of accelerated deleveraging, with characteristics typical of a crowded trade.

The most common opinion is that the trigger was the appointment of Kevin Warsh as Fed chairman, interpreted as a sign of greater monetary orthodoxy and less likelihood of aggressive rate cuts, compounded by technical factors such as increased margin requirements on futures and ETFs (CME, US and Chinese stock exchanges), seasonal sales ahead of the Lunar New Year in China and the marginal strengthening of the dollar.

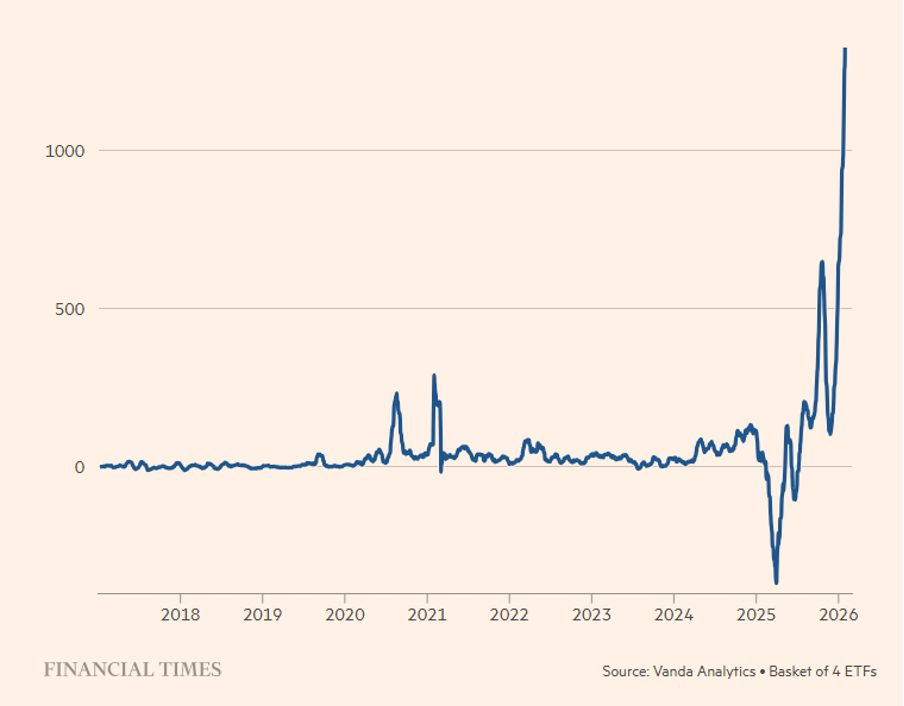

As we have already highlighted in previous Insights, the rally was built with the decisive contribution of retail buyers. In particular, for silver (see Figure 2), it was driven by record inflows of retail capital into silver ETFs (≈ $1 billion in a single month) and extreme volumes on instruments such as SLV and, above all, leveraged ETFs (AGQ -2x), which, combined with increased margin requirements, triggered a chain of margin calls, forcing investors to liquidate positions in metals and sell unrelated assets (equities), generating cross-asset contagion.

Figure 2. Net retail purchases of silver ETFs (data in millions of dollars). Amounts on a monthly basis.

Silver reacted more intensely than gold in both the expansionary and downward phases because silver is structurally a smaller and less liquid market than gold; it is more elastic to speculative flows and is historically prone to overshooting in both directions (‘gold on steroids’).

Although in the short term the precious metals market may experience further declines due to technical factors (margins, liquidations, etc.) and volatility is likely to remain high, in the long term some institutional investors see the drawdown as a cyclical correction, not the end of the bull market, primarily because the structural drivers (public debt, geopolitics, diversification) remain valid, especially for gold, while silver remains a high beta asset, more suited to opportunistic strategies than defensive hedging.

Disclaimer

This post expresses the personal opinion of the Custodia Wealth Management staff who wrote it. It does not constitute investment advice or personalised advice and should not be considered an invitation to carry out transactions in financial instruments.