A couple of months ago, the German Ministry of Finance took a significant step: it cancelled the long-planned Christmas issue of a commemorative silver coin dedicated to the ‘Three Wise Men’ and a second (less festive) silver coin dedicated to monorails.

The reason? The price of silver rose sharply in October, reaching $53 an ounce, a level at which “the material value of German 20 and 25 euro silver coins currently far exceeds their face value”, as the Ministry of Finance explained. In simple terms: issuing those coins no longer made economic sense.

Since then, silver prices have continued to rise. A few days ago, the price of silver reached $64 per ounce, almost double what it was a year ago, after the Federal Reserve cut rates by 25 basis points.

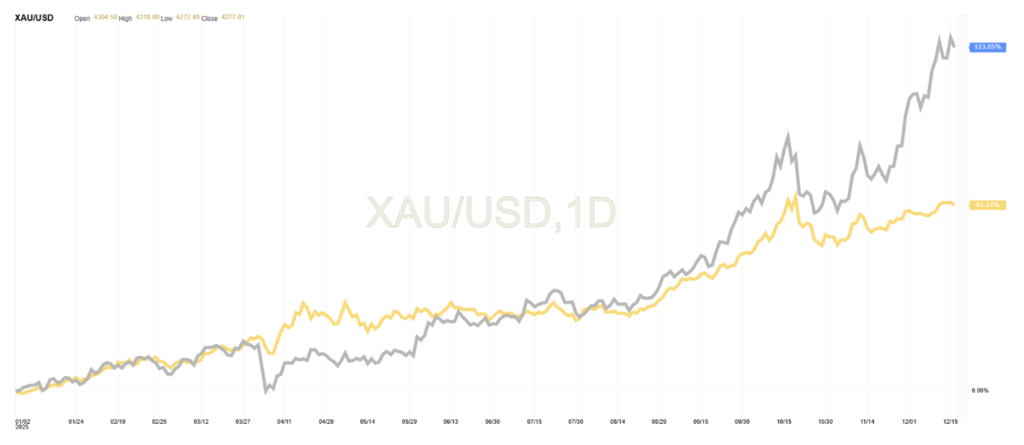

Figure 1. Comparison between the performance of silver (gray line, approximately +113%) and gold (yellow line, approximately +60%) for 2025.

This figure easily exceeds the approximately 60% increase in gold prices recorded this year, not to mention that it is gold that has attracted all the attention. In fact, the increase in the price of silver has been so marked that such a rise has only occurred twice in recent history: in the late 1970s (against a backdrop of oil and inflation shocks) and in 2008 (during the global financial crisis). We were used to seeing this kind of performance only with Bitcoin!

Similar to gold, the surge in silver prices did not coincide with a stock or bond market crash. At best, this makes the pattern unusual and, at worst, potentially threatening. We will not delve into the analysis of the other two precious metals, platinum and palladium, whose prices are also influenced by industrial dynamics, with platinum gradually replacing palladium in the production of catalytic converters. Gold and silver, on the other hand, have more similar destinies, as their industrial uses are marked by jewelry and electronic components.

How can this phenomenon be explained? The answer lies in a mix of fear and greed, coupled with rising levels of speculation. Let’s start with greed: over the past year, industrial demand for silver has risen steadily, particularly from sectors such as electric vehicles and computer chips. If history teaches us anything, this will eventually lead to an increase in supply (i.e., increased mining).

But since this cannot be achieved quickly, supply and demand are currently out of balance. And this imbalance has become doubly intense because the White House recently designated silver as a strategic commodity, sparking fears of imminent customs duties, a threat that tends to exclude gold.

This has led to a build-up of stocks within the US. This in turn has exacerbated the shortage elsewhere, creating strange price gaps between London and New York. And, predictably, there are rumors that some savvy financiers have exploited this gap. It is a dynamic similar to that of copper, which we illustrated in our Insight of July 11, 2025.

If so, this would be a pale echo of the speculative distortion—that is, price distortions caused by aggressive traders seeking to make profits—that erupted in 1980, when a group of investors known as the “Hunt brothers” triggered a (notorious) squeeze on the silver markets. Nelson Bunker and William Herbert Hunt, Texas oilmen, realized in 1979 that the silver market was limited and circumscribed and that if they had the opportunity to acquire a substantial share of it, becoming oligopolists, they would make a fortune, as they could influence the supply side of silver and determine its prices. They managed to grab a third of the total supply (excluding the share held by central banks and governments), alarming jewelers such as Tiffany and the commodity exchange (COMEX) itself, which reacted by raising the margins on futures contracts (the famous Silver Rule 7) and causing a chain reaction of sales by small operators and a relative drop in prices. heavily indebted to purchase physical silver, the Hunt brothers were no longer able to honor their margin requirements or the loans taken out for their speculations, triggering panic in the silver markets: it was March 27, 1980, which went down in history as Silver Thursday. To end the panic and save the situation, a consortium of banks provided the brothers with a $1.1 billion line of credit so that they could meet the margin call and fulfill their financial obligations. In 1988, the brothers were found civilly liable for their attempt to monopolize the silver market and were ordered to pay $134 million in compensation to a Peruvian mining company that had been severely damaged by their actions.

There is also a third factor behind the surge in silver prices: retail investor mania is on the rise, as the Bank for International Settlements noted this week. In particular, the sense of “FOMO” – or fear of missing out – is driving investors to bet on sectors related to artificial intelligence, as well as gold and cryptocurrencies. And as the prices of these assets have risen, some investors now seem to be turning to silver as well, not least because they realize that silver has real uses, unlike many other speculative assets. This has made it doubly attractive. Silver, if you will, is the new “useful” gold. But be careful: when we talk about investors, we often have to deal with cognitive biases that have been extensively studied by behavioral finance and that also characterize sophisticated investors, who sometimes lose sight of the data (when available) and create altered representations.

Then there is fear. With the Fed cutting rates three times this year, even though inflation exceeds its 2% target, there is growing concern about “fiscal dominance,” i.e., that governments will force central banks to cut rates to make it easier to service their ever-growing debt. This has pushed up long-term bond yields in the US—and elsewhere—in 2025, even as short-term rates are falling, leading some investors to embrace bullion (including silver) as a “devaluation play,” or a hedge against the risk that inflation or even default will erode the value of fiat currencies.

And, as financial historians might note, there is certainly no guarantee that silver—or gold—is a more reliable asset. On the contrary, silver prices have been so volatile in the past, due to the market’s lack of liquidity, that traders joke that the precious metal is “the widow maker” because it can cause large losses. The Hunt brothers are a case in point: after the dramatic price rise in 1980, prices collapsed, wiping them out.

This could happen again. But for now, fear and greed continue to rage, intensified by uncertainty over what the US president might do to the Federal Reserve or with tariffs. In this sense, therefore, the aborted Christmas coin is a powerful sign of our times, in which exuberance and unease are now intertwined in the markets, albeit not quite in the form of ‘commemoration’ desired by the German Ministry of Finance.

Disclaimer

This post expresses the personal opinion of the Custodia Wealth Management staff who wrote it. It is not investment advice or personalized advice and should not be considered an invitation to carry out transactions on financial instruments.