In our previous Insight, we emphasised that US insurance companies were among the main investors in private credit, highlighting a dangerous systemic risk. Global life insurance companies manage approximately $25-30 trillion in AUM, representing around 8% of global financial assets. Clearly, a problem in this sector could have wider repercussions for global financial stability.

Given their profile as financial institutions with long-term liabilities, private credit is a perfectly sensible allocation because a long-term investment horizon allows them to benefit from the illiquidity premiums offered by this asset class.

At present, however, there are three main concerns regarding these investments.

1) Private credit markets have experienced rapid growth in recent years in terms of performance, at least in part due to weaker underwriting.

2) Insurance companies’ allocations to private credit are generally increasing.

3) Some insurance companies are owned by private equity firms that originate private credit, adding potential risks to a system that could already be considered somewhat opaque if private equity-owned insurance companies invest in private credit originated by their shareholders.

It is comforting that the private equity ownership of life insurance companies in Europe remains moderate, at less than 10% of share capital, according to the Bank for International Settlements. This compares with around 25% for US life insurance companies and around 5% for Asian life insurance companies.

We share some of the concerns of global regulators, particularly with regard to the private equity ownership model. However, to date, private equity ownership in European life insurance has been moderate and regulators are vigilant about the risks involved; in our view, this should not be the focus for bond investors in European life insurance companies. Contagion to European insurers is the main risk that needs to be closely monitored should we see further pressure in the US sector, which is the real problem.

We would add that, in our opinion, the problem is not limited to the insurance sector. The banking system, particularly in the United States, is also involved in this market to a worrying extent and in worrying ways. It is true – and we reiterate this – that banks are subject to constraints that prevent them from investing directly in this asset class, but this does not mean that they cannot do so indirectly: this is what we want to clarify below.

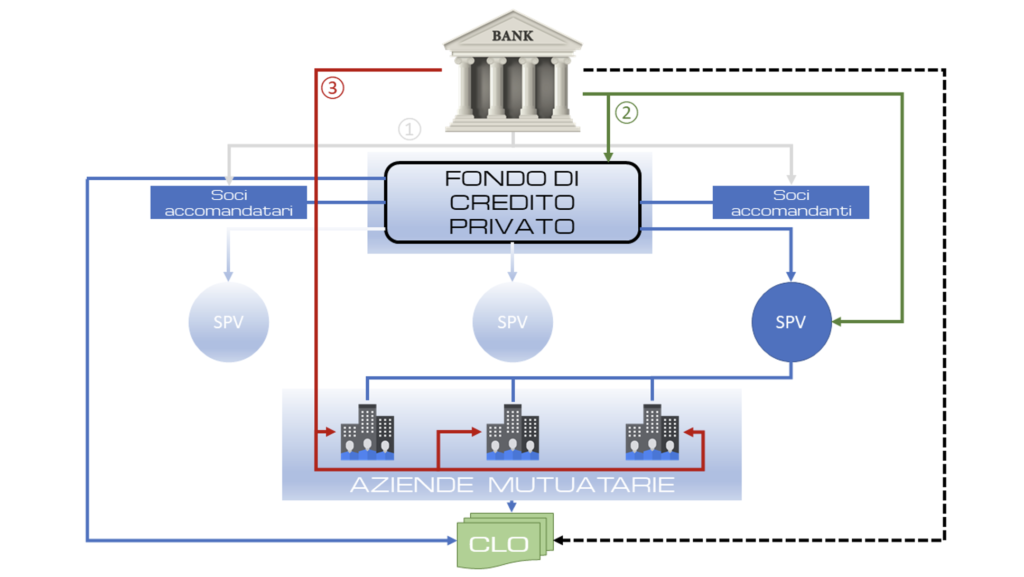

Lenders and private credit funds have intertwined their destinies, with banks granting hundreds of billions of dollars in financing, increasing the returns of private credit funds. Banks provide the infrastructure for the trillion-dollar private credit market, offering leverage and liquidity throughout the life of a fund. In the chart below (Figure 1), we show how banks can finance private credit on three levels:

1) By financing investors in a private debt fund

2) By financing the fund and/or Special Purpose Vehicles (SPVs) used by private debt funds

3) By directly financing individual companies (which would be the commercial bank’s business).

Figure 1. Levels of participation in private debt financing by the banking system.

At level 1), both limited partners and general partners can be financed. Limited partners, usually large institutions such as pension funds, endowment funds and insurance companies, are those who provide the capital to be lent. The general partner is the private credit company that manages the fund. Both can obtain loans from banks. Limited partners can obtain loans from banks to finance their commitments to the funds, while general partners can obtain loans against the commission income they receive from managing the funds on behalf of institutional investors.

Then there is the fund itself: level 2). Once it has obtained commitments from limited investors, it can begin to obtain loans through so-called underwriting lines, using the investors’ commitments as collateral. These revolving lines of credit allow funds to invest money more quickly, without waiting for investors to pay in cash.

Underwriting lines are also popular because they help amplify performance, as the industry’s “internal rate of return” metric is calculated from the date the investor’s money is invested, rather than the date the commitment is made.

Once the funds have been obtained, the private credit fund can:

• Grant loans to borrowers and then approach banks to obtain additional financing using those loans as collateral.

• Use the fund’s entire net worth as collateral: NAV lines, as they are called in the industry, can be used to repay investors early, further shortening the time period over which returns are measured and amplifying performance, or to free up capacity for new loans. NAV lines have been controversial, with regulators calling them ‘leverage on leverage’ because the fund borrows against the value of existing investments, which already use large amounts of debt.

• Tap into the large market for loans issued through collateralised loan obligations (CLOs), which is estimated to be worth around $1.5 trillion. To create a CLO, the loans issued by the fund will be pooled and divided into tranches, which will then be sold to investors based on their risk appetite. Investors in CLOs are typically insurance companies, pension funds and sovereign wealth funds, which also invest in private credit funds, as well as banks. The CLO will need a large and diversified pool of loans, so the SPV of a private credit fund will use a form of temporary financing from a bank, called a warehouse line, until there are enough loans to fill the pool. Most of this debt is floating rate, which makes borrowers vulnerable to rising interest rates, and is secured by loans to companies that are already heavily indebted. CLOs are a little more dangerous because they tend to have higher leverage and there is an implicit bet that CLO markets will remain open and that guarantees will continue to function. At the same time, banks are transferring part of the risk on their loan portfolios to private credit funds through transactions known as significant risk transfers.

The market for packaged and repackaged debt is the most attractive to the banking sector, as sub-prime mortgages have shown us (see the dotted connector in Figure 1). Banks repackage their loans and purchase protection from investors against defaults on the riskiest parts, which they agree to pay if things go wrong in exchange for a quarterly fee.

Significant risk transfers have been around for a long time and were mainly used for traditional assets such as corporate loans or mortgages.

But banks’ most profitable customers are private equity and credit funds, so they are increasingly setting up transactions in which they offload the risk associated with underwriting lines and NAV loans to increase their lending capacity to the sector.

Private credit funds represent an increasingly important part of the group selling protection against losses on these loans. They also use leverage for these transactions, often provided by the banks themselves, raising concerns and doubts about whether the risk is actually being transferred out of the banking system.

Moving on to the operational arm of the funds, SPVs, their financing generates indirect leverage. The private credit fund owns the SPV’s equity, but the low-default-risk vehicle is separate from the fund (asset segregation). This allows banks to “ring-fence” assets and understand exactly which loans serve as collateral at any given time.

New loans originated by the fund are transferred to the SPVs and used as collateral for what is known as “loan-on-loan” financing, for the simple reason that the funds are taking out loans to finance new ones. These loans tend to be “over-collateralised”, meaning that SPVs borrow less than the value of the assets pledged as collateral. However, there is still a risk that the loans will deteriorate rapidly and that, at the same time, banks will suffer losses.

A single fund may have dozens of these SPVs if it draws on the leverage of several banks (ideally, one SPV per bank), each of which holds a pool of revolving loans.

A bank typically advances 60% to 70% of the value of the loans placed in the SPV. The bank relies on the diversification of the loan pool to protect itself from losses, as well as on the collateral on the loans.

The financing bank receives data on the underlying performance of each loan and evaluates it at its sole discretion. If it finds a weakening in performance, it can remove a loan from the SPV and require the fund to replace it with a performing loan. The bank may also decide to reduce the size of the credit line, limiting the leverage granted to the private credit fund.

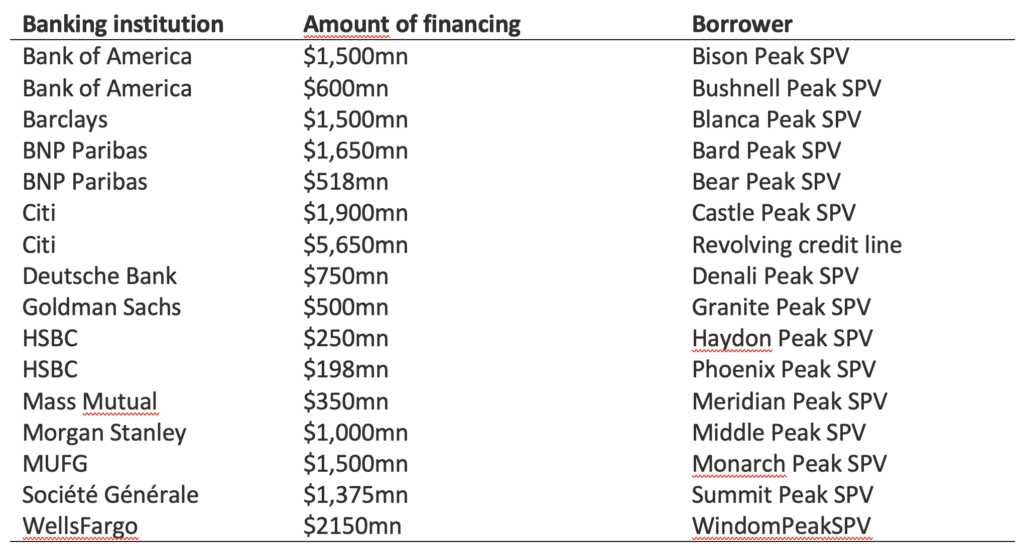

As an example of this market segment, we report the available data on bank financing to the SPVs of Blackstone’s private credit fund, which can be consulted in Table 1.

Table 1. Blackstone private debt fund SPVs. Source: BCRED archives.

Another form of financing for SPVs is repos, where the SPV sells a group of loans to a bank with the agreement that the bank will repurchase them at a premium at a later date. Repos tend to involve daily margin requirements and are therefore traditionally used for ultra-safe and liquid assets such as government bonds.

However, the fund and the bank can negotiate their own terms bilaterally, making the repo market notoriously opaque. Repo contracts can be used for a pool of loans or even for a single loan, but it is almost impossible to know how widely this type of financing is used by private credit funds.

Regulators, such as the European Banking Authority and the Bank of England, have complained about “black holes” in the data and are asking banks for greater transparency on repo financing. One concern is that the link between private credit funds and the repo market – used by financial institutions to meet their short-term financing needs – could increase systemic risks when repos are linked to illiquid private debt that must be sold quickly in times of stress.

Level 3) involves lending directly to the target companies of the fund and its SPVs. Both banks and private credit funds argue that it is unusual for them to lend to the same companies. But last year, the ECB stated that this could be because lenders do not necessarily monitor this phenomenon. The inability to correctly identify, at an aggregate level, exposures to companies that also borrow from private credit funds means that this exposure is almost certainly underestimated and the concentration risk cannot be adequately identified and managed.

Far from wanting to spread alarmist views on the situation of the financial markets, we are reporting facts that tend to liken the current market situation to that of the pre-crisis period of 2008, well aware that analogies are often misleading because a financial crisis never repeats itself in exactly the same way as a previous one, simply because it develops in different contexts. Therefore, our approach is and will continue to be to report risk factors – in this case systemic ones – without overemphasising the similarities.

Disclaimer

This post expresses the personal opinions of the Custodia Wealth Management staff who wrote it. It does not constitute investment advice or personalised advice and should not be considered an invitation to carry out transactions on financial instruments.