A question whose answer is as precious as gold.

The most common answer to this question is that gold is a safe haven asset that protects against inflation. However, it is easy to argue that gold is not an asset that has a strongly negative correlation with inflation, so only in the long term can it protect the real value of wealth, just as stocks and real estate do.

Even the argument of non-correlation with major asset classes such as stocks and bonds is not one that has a solid statistical basis. We hope we have clarified in a few lines why it is so difficult to answer the question we have asked ourselves.

We found an interesting article on the World Gold Council that provides an intriguing answer to this question. The added value that an allocation to gold brings to a portfolio lies in the “bridge” role that this asset class plays between alternative and traditional investments (stocks and bonds, to be clear) or – to use the terminology of the aforementioned article – between public and private investments, meaning publicly traded (and therefore liquid) instruments and (relatively) illiquid instruments such as hedge funds, private equity, and private debt. An allocation to gold (whether through passive instruments or through an investment in physical gold) has three clear benefits: liquidity, return, and volatility. If we consider these three variables as continuous in their domain of definition, gold exists in this continuum, not because it mimics public or private assets, but because its characteristics embrace both. It is traded with the liquidity of public markets, but behaves with the defensive stability that investors often seek in private strategies. In portfolios that balance public and private allocations, gold becomes a natural trait d’union. As portfolios are tested through various cycles, gold provides the quiet strength that keeps the foundations solid. While portfolios are put to the test in various cycles, gold provides the silent strength that keeps the foundations solid. This phrase may seem a little too lyrical and not practical enough, but it accurately captures the meaning of the analyses conducted in the article, which we will outline below.

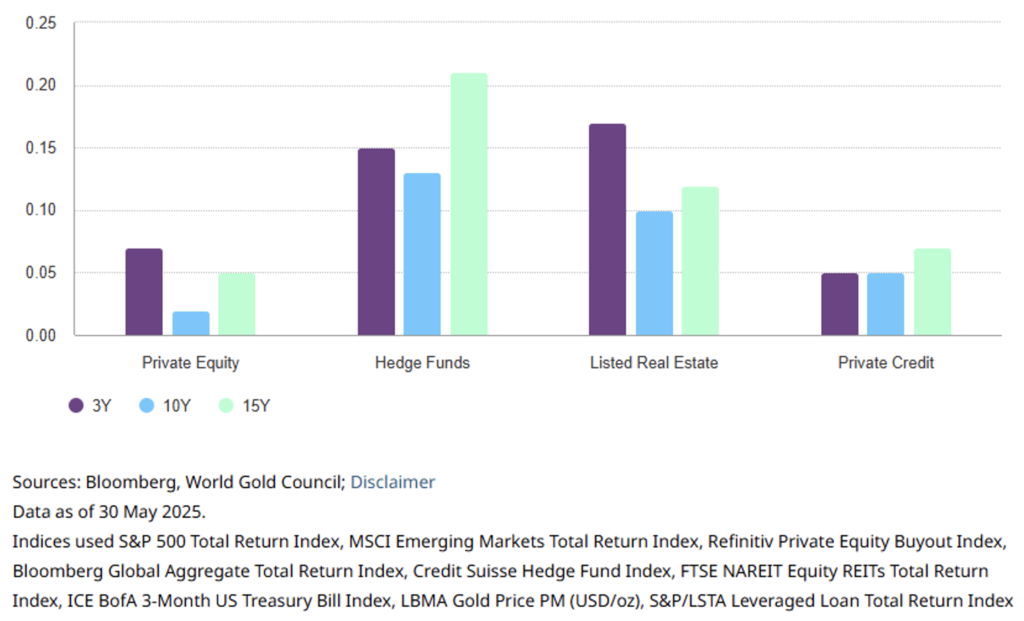

Let’s see how gold interacts with alternative investments. Let’s start with correlations and look at Figure 1.

Figure 1. The correlation between gold and alternative instruments remains low over time.

The most marked correlation—which, however, does not exceed 0.25—in the long term is between gold and hedge funds, which, coincidentally, are the most liquid alternative investment. But beyond this, the main reason for this result lies in the fact that CTAs, global macros, and trend followers, more generally, tend to be buyers of gold when it shows momentum. This could well explain a slightly higher correlation coefficient.

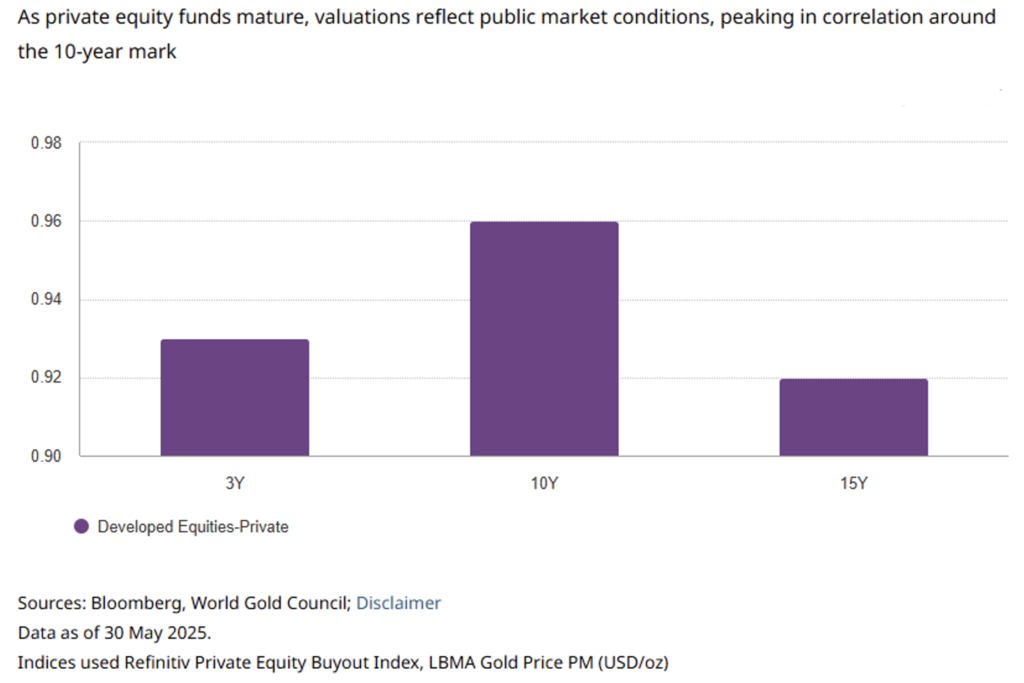

With private equity, on the other hand, gold is virtually uncorrelated, whereas private equity tends to correlate almost perfectly with listed equities (see Figure 2).

Figure 2. Private equity becomes increasingly correlated with public markets over time.

Correlations between public and private equities have been high and have increased over the medium to long term due to the life cycle of funds. As the fund cycle matures, private equity valuations tend to align more closely with those of public markets. The underlying companies in the portfolio are revalued more frequently as exit strategies, such as IPOs, become clearer. As a result, valuations align more closely with prevailing market conditions, pushing the correlation upward around the tenth year, then easing slightly in the fifteenth year, when funds mature and residual assets become less sensitive to the market.

An alternative asset class of recent interest is private debt, i.e., lending strategies that do not fall within traditional banking channels. Private debt strategies cover a broad spectrum, from senior secured loans to opportunistic and distressed debt, allowing investors to tailor their exposure to their return objectives and risk tolerance. The trade-off, however, is illiquidity and less frequent revaluation, which can obscure the volatility of their value over time and dampen that of the portfolios in which they are held during periods of stress.

This asset class has gained importance, initially in a low interest rate environment when investors were seeking yields, and more recently in a context of ongoing regulatory change, with banks reducing the leverage of their balance sheets in response to Basel IV.

A typical private debt portfolio combines elements of capital preservation and yield enhancement, often through a mix of senior secured loans and opportunistic strategies. When gold is added to such a portfolio, risk-adjusted returns improve. Gold acts as a liquidity reserve and risk management tool, particularly valuable during credit market turmoil when traditional hedges, such as government bonds, may be less reliable.

As investor interest in private debt continues to grow, developments in the broader leveraged finance market, particularly collateralized loan obligations (CLOs), may offer insight into the transmission of credit stress (credit crunch) that could eventually manifest in private portfolios. This reinforces the need to hold liquid reserves, such as gold, to manage financing needs and portfolio shocks when private asset valuations adjust with some lag. Although CLOs and private debt differ structurally, they share a similar borrower base. Signals from CLOs, such as increased exposure to CCC ratings or a contraction in junior overcollateralization (OC) reserves, can serve as early warning indicators of debt deterioration.

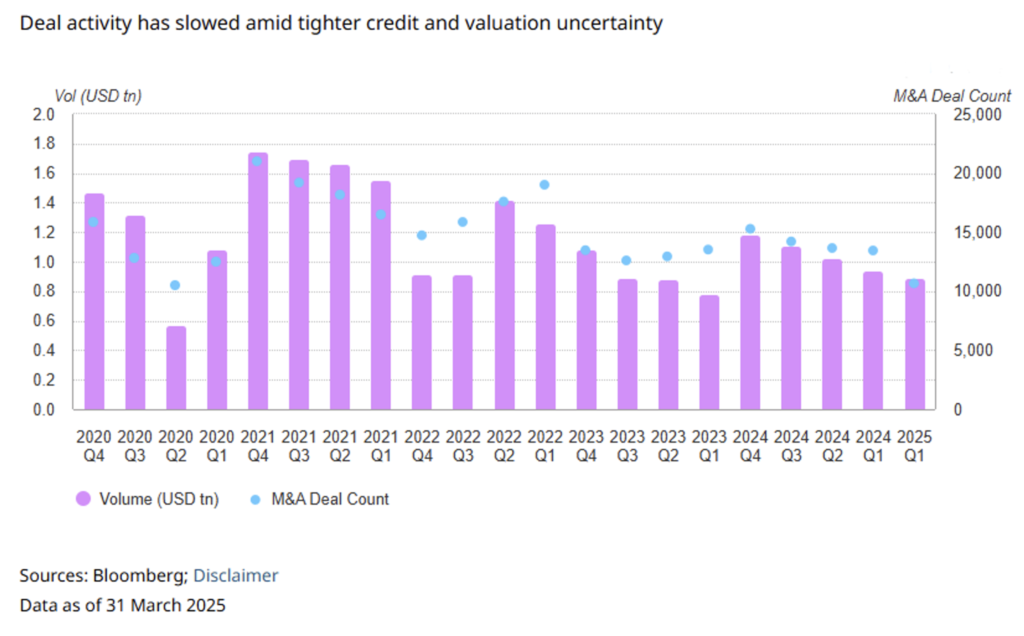

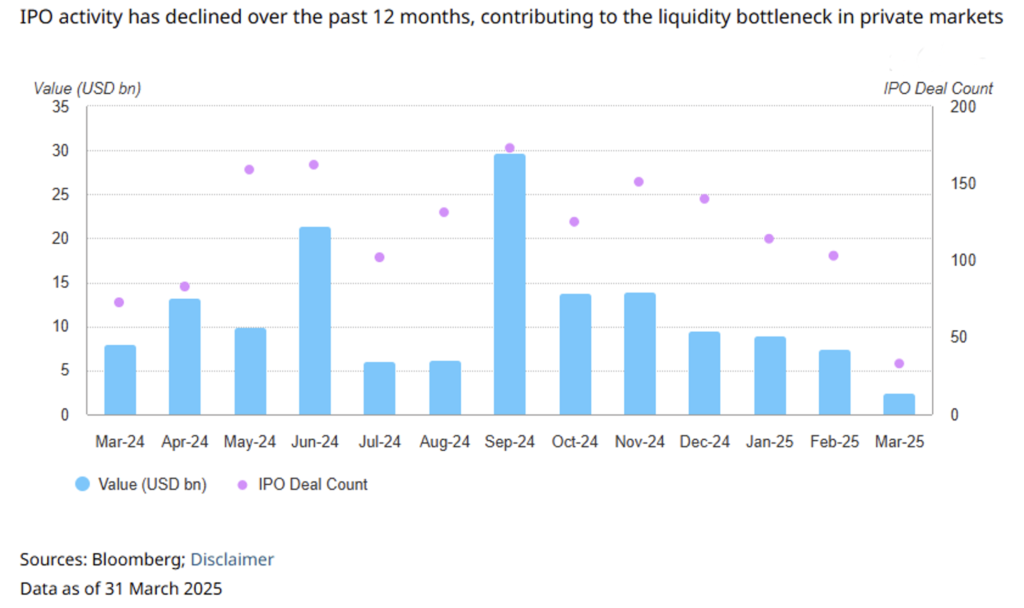

In the M&A world, gold can act as a buffer in a market that is clearly in crisis. Both the number of transactions and volumes are declining. Once a reliable source of liquidity (and returns), IPOs have lost momentum, contributing to a slowdown in exits (see Figures 3 and 4).

Figure 4. Over the past 12 months, there has been a slowdown in IPOs in terms of exit dynamics.

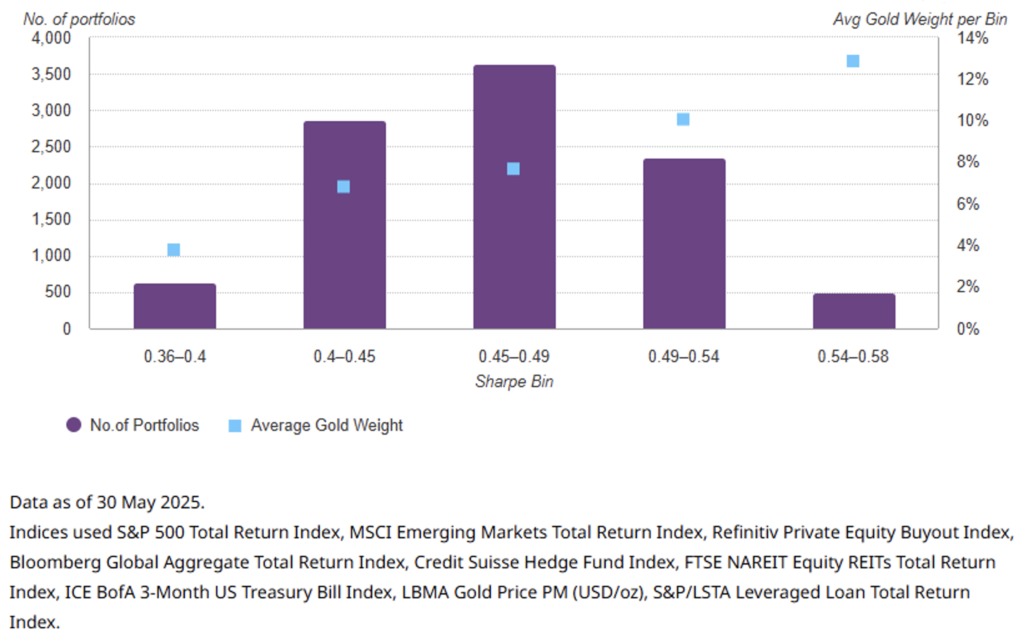

If we add that gold, when appropriately allocated (where appropriately means with weights ranging from 5% to 8%) in a mixed portfolio of traditional and alternative assets, contributes to increasing its efficiency as measured by the Sharpe Ratio (see Figure 5), then we conclude that the yellow metal is a beneficial asset for a “diversified” portfolio. But let us reiterate once again: it is the hybrid nature of gold as a partly traditional and partly alternative asset that confers this efficiency premium. Unless you wish to dispute the methodology used to conduct the analysis in the article we have cited, which we have limited ourselves to summarizing, we hope to have made an original contribution that highlights what we believe to be the most solid reason for investing in the precious metal par excellence.

Figure 5. Average weight of gold by Sharpe ratio range.

Disclaimer

This post expresses the personal opinion of the Custodia Wealth Management staff who wrote it. It is not investment advice or recommendations, nor is it personalized advice, and should not be considered an invitation to carry out transactions on financial instruments.