Undoubtedly no one have missed the new record set by the price of gold in the last week: more than $3’000 per ounce. This skyrocket growth of the yellow metal is undoubtedly due to its universally recognized characteristic of being a safe haven asset capable of preserving value against the turmoil that characterizes other assets and the action of inflation that the tariff war inevitably vows to sharpen in the near future. This statement stems from the fact that the other highly liquid (in the sense of highly traded) precious metals namely silver, platinum, and palladium have not exhibited similar dynamics (at least not in the last 15 years).

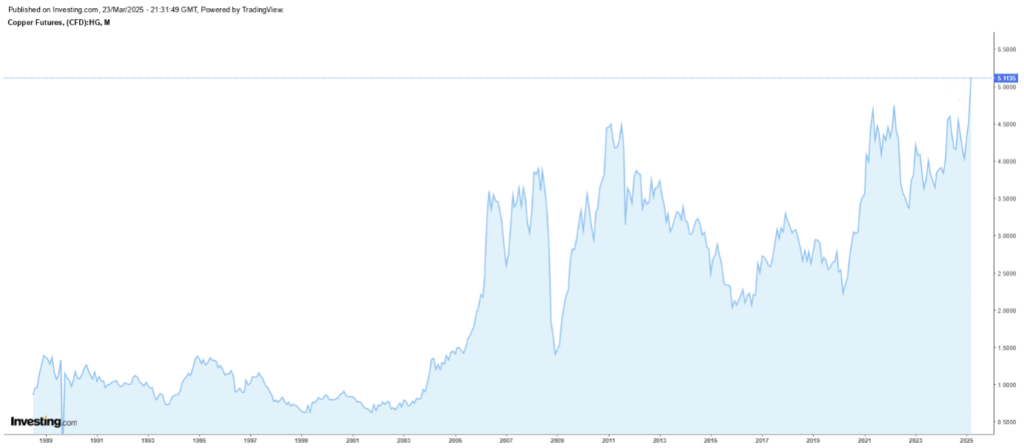

But there is another metal that is exceeding its all-time highs these days: copper.

The future on copper listed in COMEX (HG) from 1989 to today.

Obviously, in this case, we are talking about a completely different category of metals having the red metal a primarily industrial use. It belongs to base metal category which is define in chemical sense as being of medium reactivity somewhere between the very reactive alkali metals and the unreactive precious metals. In the commodity market parlance what matter is the liquidity of the asset which is in the middle of very liquid metals like gold and very illiquid ones like cobalt. Definitely copper, like all the other most traded base metals (aluminum, nickel, zinc, lead, and tin) is not a safe haven asset and therefore its value is determined by its industrial uses which spam from residential and commercial construction wiring and plumbing to application as a material to fabricate heat exchangers (a core functionality for cooling chipsets in computers, electronics, air conditioners and refrigerators).

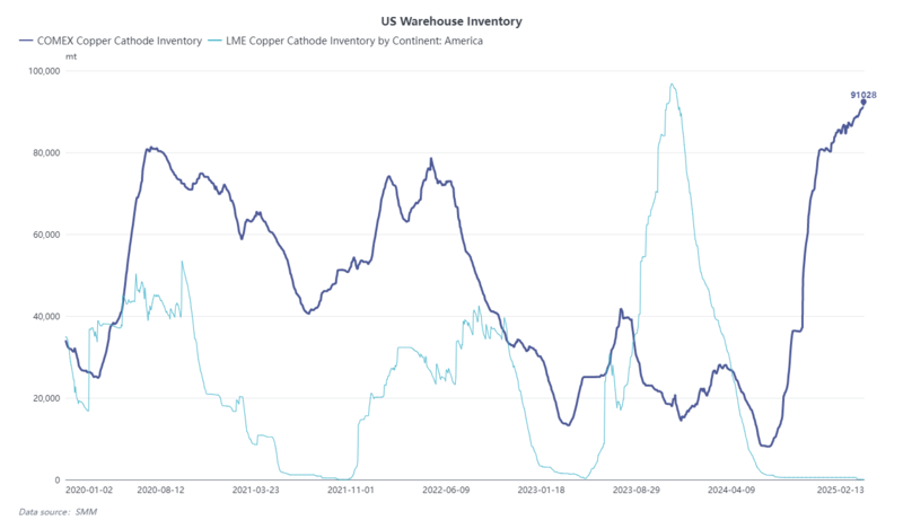

This being said, it is not surprising that the rise in copper prices has a completely different cause compared to gold: i.e., the tariff war. Levies of 25 per cent have already been introduced on all aluminium and steel imports and the charge of the same percentage was announced by the Trump administration. This triggered a rush to export copper to the United States because once stored in the US Comex warehouses the stock of imported metal benefits of the so-called “duty paid” basis, meaning any taxes and levies on the metal must have been settled. As a result, copper in those facilities would not be hit with additional tariffs.

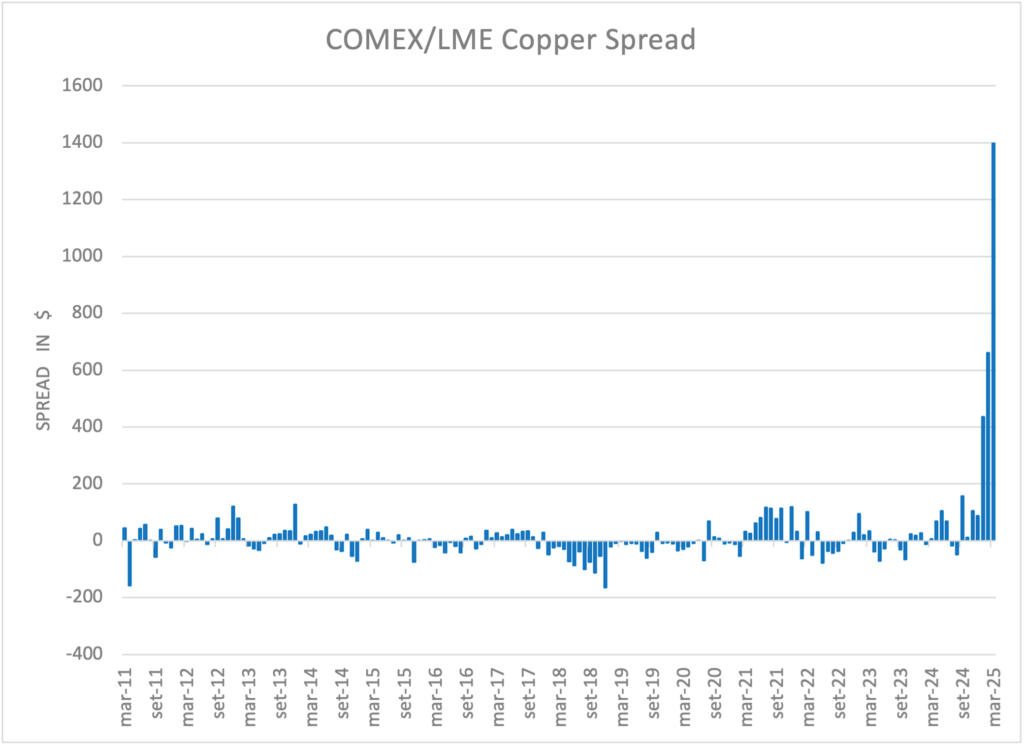

But there is another consequence of the tariff war. The abnormal increase in the spread between US and UK copper.

First of all, the red metal quotes in pounds in COMEX and tons in LME. Therefore, in order to compare both futures we need to convert metric tons to pounds: the ratio is 1:2204.62. Then we can calculate the spread and see that it is growth to never seen levels (about $2000 intra-month). In order to deliver as much copper as possible to the U.S. before the duty was applied, the price dropped considerably compared to the U.S. price due to an increase in supply.

In addition, the red metal is experiencing a supply contraction partly driven by very high prices and partly justified by very low smelting fees due to competition from Chinese smelters in the first place. This discourages a production increase.

Since spreads are typically mean reversal processes there might be a temptation to bet in favor of narrowing this spread. However, we point out that, globally, there is such a shrinking supply of the red metal that caution is advised in this type of arbitrage.

Disclaimer: This article expresses the personal opinions of the contributors of Custodia Wealth Management who wrote it. It does not constitute investment advice, personalized consulting, or an invitation to perform transactions on financial instruments.