Why would tariffs on imports to the United States, mainly imposed on Canada and Mexico, and to a lesser extent on China (which are already subject to suspension and renegotiation), affect global car sales?

A first answer lies in the extreme interconnection of the supply chain: many components are assembled abroad, even though they are produced in the United States.

The most exposed are three major US car manufacturers – GM, Chrysler, and Ford – because part of their production takes place in Mexico and Canada. Europe, although not yet affected by the tariffs, will also suffer repercussions: automakers such as Volkswagen produce about half of the vehicles intended for the US, Mexican, and Canadian markets.

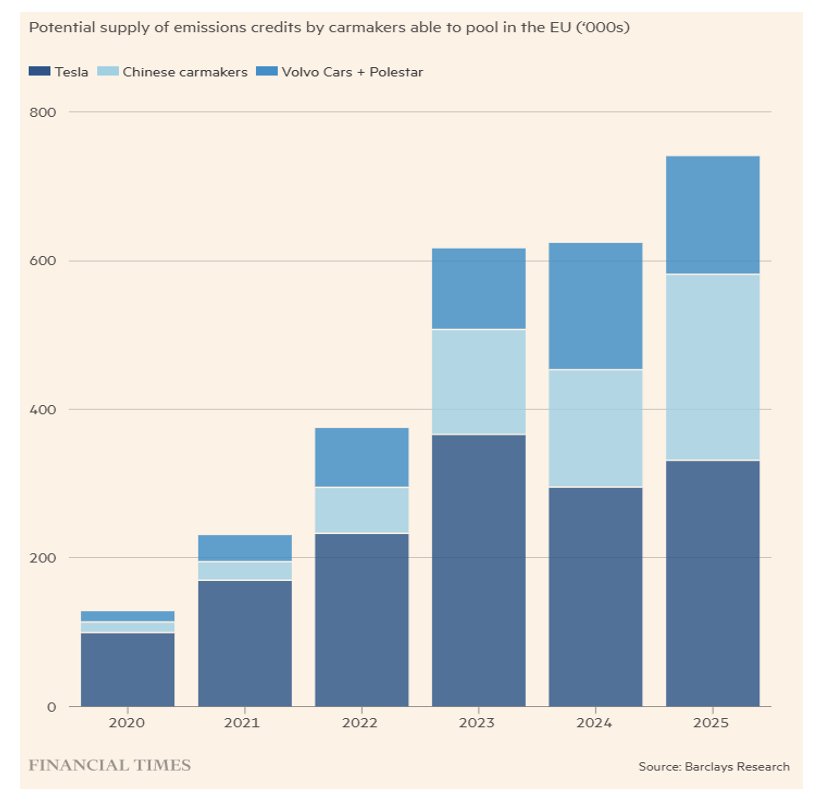

The self-defeating approach of the European Commission should also not be overlooked, as it plans to fine car manufacturers producing in Europe – with Volkswagen being the most exposed – by charging 95 euros for every gram of CO₂ emitted per kilometer. This would force manufacturers to sell more electric cars (but at what cost?) or to offset their greenhouse gas emissions through “pooling”, i.e., collectively selling their fleet together with more eco-friendly subsidiaries to stay within the impunity threshold.

However, there is also a third option: purchasing carbon credits to compensate for excess CO₂ emissions. The largest portfolio of these green certificates undoubtedly belongs to Tesla, now closely pursued by Chinese electric car manufacturers such as BYD.

Nevertheless, Tesla is not doing well. According to Barclays analysts, the company produces between 20% and 25% of its components in Mexico, not to mention the threat of retaliatory tariffs announced by Canada, specifically targeting Tesla.

These possible scenarios highlight how difficult it is to make accurate predictions, given the globalization and complexity of the automotive market. However, as already happened during Trump’s first presidency, explicit threats amplified by a resounding echo were often followed by negotiations with more rational objectives. This, too, is a negotiating tactic!

Disclaimer: This article expresses the personal opinion of Custodia Wealth Management contributors who authored it. It does not constitute investment advice, personalized consultancy, and should not be considered an invitation to carry out transactions on financial instruments.