When we talk about carbon credits, an inexplicable confusion always arises. A carbon (or climate) credit is a permit to pollute (up to a certain limit) granted annually by a state authority to large, highly polluting companies (such as metal producers, airlines, chemical plants, etc.).

And here, for once, Europe and its strong tendency to regulate have contributed to creating the world’s largest carbon credit market (EU Emissions Trading System – EU ETS). According to Sparkchange, this market trades an average of 2 billion euros per day, involves more than 13,000 polluting companies (responsible for about 40% of greenhouse gas emissions in Europe), and covers approximately 1.2 billion tons of CO2 emitted into the atmosphere.

But let’s see how it works. Since 2005, each European country has been required to issue a certain number of certificates (European Allowance – EUA) each year, which are recorded in a dedicated registry maintained by each member state. Each certificate is essentially a right to pollute, meaning to release one ton of CO2 (equivalent, since not only CO2 is a greenhouse gas) into the atmosphere due to its production process. These certificates are either granted for free to some companies or purchased at auction; the auctions take place in specialized exchanges such as EEX or ICE. Each ton of CO2 emitted results in the “destruction” of a certificate held by the polluting company (in practice, it is deleted from the registry). The remaining issued certificates can be used in the following year or sold (in addition to exchanges, banks also provide channels for trading these certificates). Conversely, once the certificate budget is exhausted, additional emissions result in a monetary penalty of €100 per excess ton and the loss of the corresponding number of EUA issued the following year. This system is known as “cap-and-trade” and aims to reduce EUA emissions annually (cap) to achieve two objectives: a 55% reduction in greenhouse gases by 2030 and net-zero emissions by 2050.

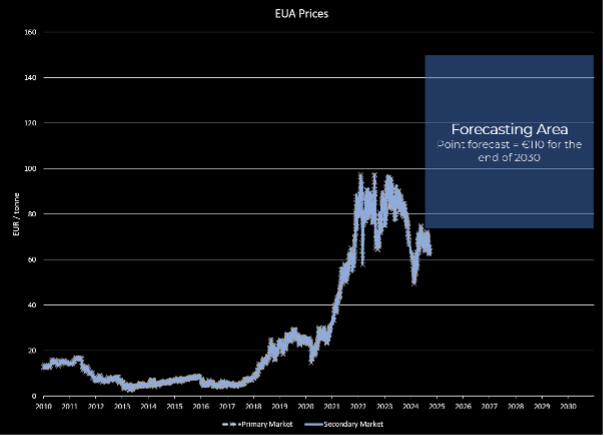

What interests us from our perspective is the trading of these instruments, which generates highly volatile prices; see the chart below for the primary market (exchange) and the secondary market (banks).

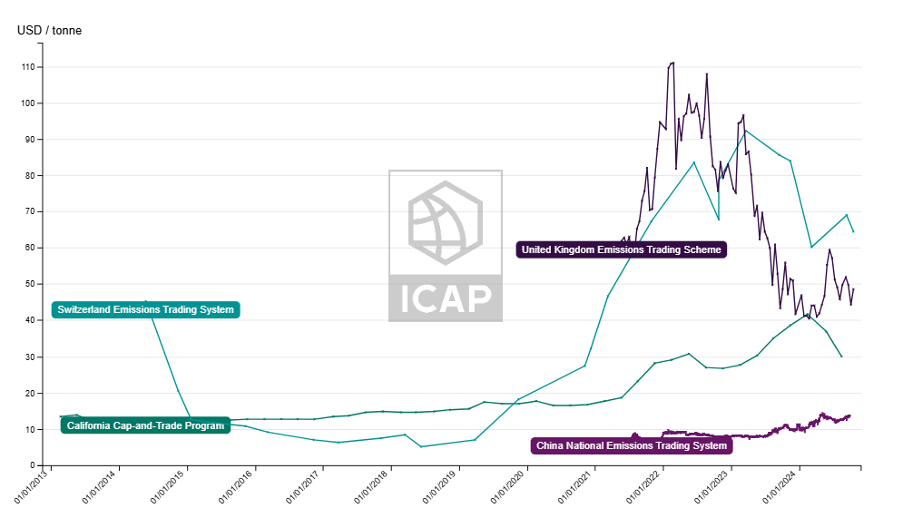

The almost perfect match between primary and secondary prices indicates the absence of arbitrage, making it a sign of an efficient market. To give an idea of why the European market is the largest carbon credit market in the world, we also present the following chart illustrating the trend of these instruments in other markets.

Framing these instruments in a standard asset class is very difficult. Considering them as a commodity seems somewhat forced: pollution does not seem like a commodity worthy of being produced. It is undoubtedly a new asset class whose prices depend on macroeconomic determinants such as production levels (including renewable energy production, which has a decreasing effect), climatic factors such as temperature, or contingent factors such as wars or pandemics. Certainly, plausible scenarios of increased energy demand (partly driven by the expansion of data centers) lead many operators to forecast prices between €110 and €150 per ton by 2030.

This is evidently a “mandatory” market, associated with “voluntary” markets with different types of instruments (which we will discuss in a future post), presenting unique issues and even higher risks. The good news, however, is that there are active and passive products on EUA or derivatives (futures and options) with EUA as underlying assets that allow coverage of long certificate positions.

Disclaimer: This article expresses the personal opinion of Custodia Wealth Management contributors who wrote it. It is not investment advice or recommendations, nor personalized consultancy, and should not be considered an invitation to conduct financial transactions.