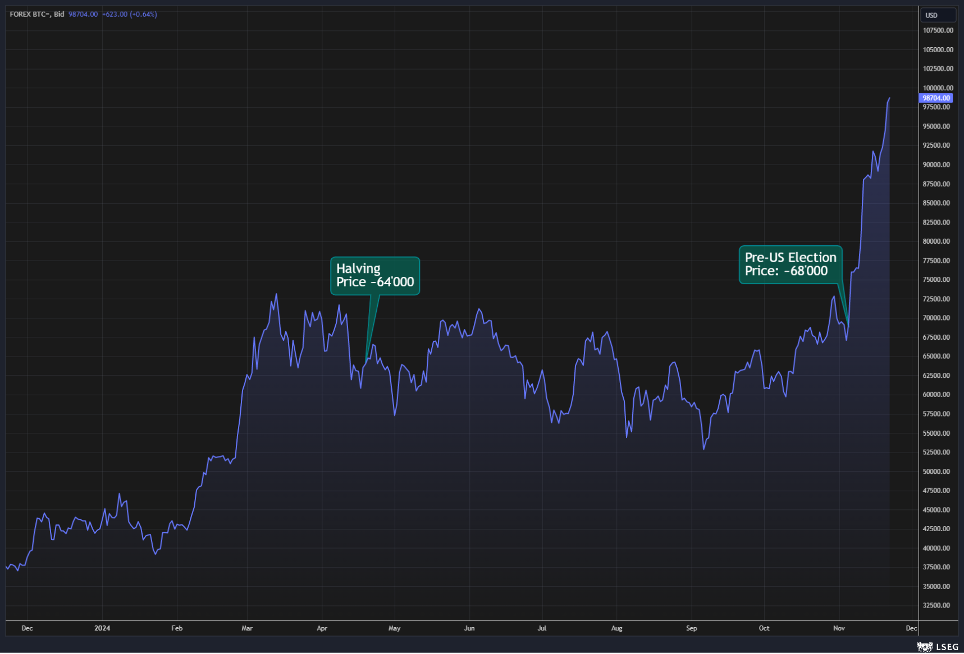

An event that dominates the headlines – not necessarily financial ones – these days is the exponential growth of Bitcoin. We have gone from around $68k before the U.S. elections to $98k as of yesterday, marking a 44% increase in two weeks (today we almost hit $100,000). We should note that in conjunction with the 4th halving of the reward per validated block (halving), which decreased from 6.25 BTC until April 19, 2024 (the date on which block number 840,000 was mined, meaning 210,000 blocks since the 3rd halving on May 11, 2020, as this is the “logical” rather than chronological clock leading to the halving) to 3.125 BTC, Bitcoin’s price was around $64k, only 6% lower.

The dominant narrative is that there has been a Trump/Musk effect, as their support for cryptocurrencies has fueled a buying frenzy—but a frenzy for what? Certainly for Bitcoin and some altcoins like XRP or Solana, but not as pronounced as BTC. In fact, among the few investable cryptocurrencies, based on the validity of the blockchain technology they are native to, only a handful—besides Bitcoin—have decisively “broken” all-time highs to test uncharted price levels.

The question is: why? How many times in discussions with friends or clients have we heard that Bitcoin (and thus other cryptocurrencies) has no intrinsic value and therefore cannot be compared to an estimate of its fundamental value (as is the case with stocks, for example), making its price movements inexplicable? Or – a more respectable position – how many times have we heard the phrase: “I don’t understand this stuff, so I don’t invest in it.”

To address the second objection, we need time and a great deal of effort to build a proper education on the subject. It is undeniable that such a complex technology cannot be understood through simple blog posts or newspaper articles, let alone its economic and financial implications. But regarding the question of value, we can already provide a reasonable answer.

Bitcoin – just like other cryptocurrencies and any other digital asset generated and traded on a blockchain – does not have a fundamental value. Like many “technological” products, its value depends on the so-called “network effect.” Think of a social network (such as Facebook or X): its value depends on the number of users who use it; intuitive, right? But this also applies to stock exchanges: what sense (and value) would an infrastructure set up to trade securities have if it had few or no users? Few users trading assets through interpersonal contacts. It is the increasing adoption by larger communities that gives value to certain realities, among which we can certainly include blockchains.

Therefore, we should not ask ourselves what the fair price of Bitcoin is or what its target should be. These are all wrongly posed questions. Instead, we should ask what the “drivers” are that lead to the more intensive use of the blockchain that interests us as investors and increase the number of its users. Among these drivers, we can mention the number of wallets, which in turn depends – in part – on the number of ETFs launched on individual underlying assets. And why not, the climate of trust that certain policymakers spread regarding the instrument and its prospects? In this sense, even Trump’s election is supportive.

Disclaimer: This article expresses the personal opinion of the contributors of Custodia Wealth Management who authored it. It does not constitute investment advice or recommendations, personalized consulting, and should not be considered as an invitation to carry out transactions on financial instruments.